Class A office rents in NYC stop making sense the moment you compare neighborhoods. Сommercial Office Space for Rent

Class A office rents in NYC stop making sense the moment you compare neighborhoods.

Walk three blocks in any direction and you’ll find completely different pricing for nearly identical space. Midtown landlords still quote pre-pandemic numbers while downtown owners cut deals quietly. Some neighborhoods are drowning in sublease inventory, while others stay tight as ever.

The problem is that most tenants hunt for space using those useless citywide averages instead of understanding what’s actually happening block by block. They end up overpaying in areas where they have leverage or missing great deals in neighborhoods they never considered.

We mapped out what Class A space actually costs in every major Manhattan district with figures as of August 1, 2025 so you can stop getting surprised by wild price swings and start making more intelligent decisions about where to plant your next office.

Manhattan Still Runs the Show

Manhattan’s Class A office rents set the pace for the entire city, and the numbers tell a clear story about where your money goes furthest.

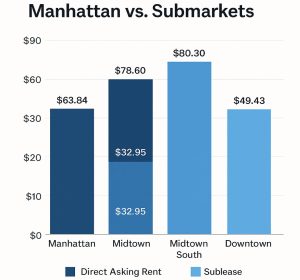

Direct asking rents average $63.84 per square foot across Manhattan, but that figure hides huge variations. Midtown commands $78.60 per square foot while Downtown sits at $49.43 – nearly a $30 difference for comparable quality space. Midtown South splits the difference at $80.30, proving creative districts still charge premium prices.

Sublease inventory changes everything. Those same Midtown spaces asking $78.60 direct? Sublease options average $32.95. Downtown sublets barely exist, keeping direct rents competitive.

Smart tenants use these gaps. Want Manhattan prestige without the sticker shock? Financial District delivers Class A space at $48.66 per square foot. City Hall area runs $47.50. Need Midtown proximity but not the trophy building markup? Murray Hill and U.N. Plaza both hover around $43 per square foot.

The vacancy rate sits at 17.5% citywide, but that inventory concentrates in specific pockets. Know which neighborhoods have options and which ones keep you competing against five other tenants for the same space.

The Most Expensive Neighborhoods

Those neighborhood variations get extreme at the top of the market, where certain addresses command the highest prices.

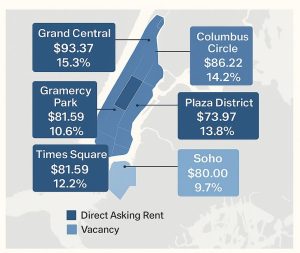

Grand Central leads the pack at $93.37 per square foot for direct Class A space. Columbus Circle follows at $86.22 direct, though aggregate pricing jumps to $89.78 when you factor in the trophy buildings.

Plaza District plays a different game entirely. Direct rents look reasonable at $73.97, but aggregate pricing hits $103.14 because landlords know they can squeeze premium tenants for flagship locations.

Gramercy Park surprises people at $86.16 direct, climbing to $95.54 aggregate. Times Square direct rents sit at $74.86, but aggregate reaches $89.90. Soho holds steady at $80.00 for direct space.

These neighborhoods command top dollar for good reasons: subway connectivity, recently renovated buildings, and tenant rosters packed with recognizable brands. That blue-chip mix keeps rents stable even when other areas soften.

Expect different rules if you’re hunting in these zones. Vacancy rates stay lower – Grand Central sits at 15.3%, Columbus Circle at 14.2%, Plaza District at 13.8%. Landlords offer fewer concessions and take longer to negotiate because they know other tenants will pay the asking price. Plan extra time if you need specific floor configurations or move-in dates.

Most Affordable Class A Submarkets in Manhattan

The flip side of Manhattan’s pricing story happens in neighborhoods most tenants overlook – and that’s where smart tenants find real value.

Murray Hill delivers Class A space at $43.21 per square foot with 24.5% vacancy. U.N. Plaza runs nearly identical at $43.34 per square foot with 22.2% vacancy. Both offer Midtown East convenience without the Grand Central premium.

Downtown plays the value game differently. Financial District averages $48.66 per square foot for Class A space but carries 25.3% vacancy, meaning landlords negotiate hard to fill floors. City Hall sits at $47.50 per square foot direct, though sublease space oddly costs more at $53.00 – a rare reversal that signals limited options. World Trade Center holds at $48.61 per square foot but keeps vacancy tight at 12.3%, so expect less flexibility there.

Higher vacancy rates in Murray Hill, U.N. Plaza, and FiDi translate directly into tenant leverage. Landlords sweeten deals with bigger tenant improvement allowances, longer free rent periods, and expansion rights they wouldn’t consider in tighter markets. Your space might cost half what Grand Central charges, but the building quality and transportation access often match up surprisingly well.

The catch? These areas require homework to separate genuinely good buildings from the ones priced low for obvious reasons.

Creative Loft Districts: Premiums for Character

While value hunters find deals in Murray Hill and FiDi, Manhattan’s creative loft districts march to their own drummer and charge accordingly.

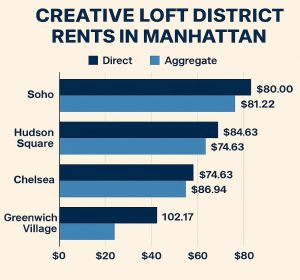

Soho leads at $80.00 per square foot direct, though aggregate pricing drops slightly to $78.74. Hudson Square hits $81.22 aggregate with 29.6% vacancy. Chelsea runs $74.63 direct but jumps to $86.94 aggregate, showing how trophy loft buildings skew neighborhood averages. Tribeca averages $74.12 aggregate with 40.8% vacancy, though limited direct inventory makes pricing unpredictable.

Greenwich Village breaks the scale entirely at $102.17 aggregate, but that reflects a handful of boutique trophy buildings rather than the broader market reality.

Flatiron and the broader Midtown South creative corridor trade in the mid-$70s to low-$80s range. Count on $74 to $77 per square foot as your working range for quality Class A loft space in Flatiron proper.

These neighborhoods hold their pricing power because agencies, tech companies, and media firms pay extra for high ceilings, unique floor plates, and the branding boost that comes with a creative address. Commodity office towers can’t replicate that combination.

Intelligent tenants expand their search radius across Chelsea, Hudson Square, and Soho to catch motivated landlords without losing the loft aesthetic. Three blocks can save you $10 per square foot while keeping the same neighborhood vibe.

Sublease Market Distortions

Creative districts might hold their pricing power, but sublease inventory turns Manhattan’s rent logic upside down in certain neighborhoods.

Midtown shows the most dramatic split: direct Class A space averages $78.60 per square foot while sublease options hit just $32.95. Columbus Circle gets even wilder – sublease space trades at $29.00 per square foot compared to $86.22 direct, creating one of the biggest pricing gaps in the city.

Other neighborhoods show smaller but still meaningful discounts. Soho sublets average $65.11 versus $80.00 direct. Penn Plaza and Garment District sublease space runs $47.57 compared to $56.77 direct.

The flip side? Several high-rent districts show zero sublease inventory. Grand Central, Times Square, U.N. Plaza, Gramercy Park, and the entire Upper East and Upper West Sides offer no recorded sublease options, which keeps their direct pricing elevated.

Speed-focused tenants can exploit these gaps, especially in Midtown and Columbus Circle, where companies dumped large blocks of older-vintage space to move fast. You might get furniture and IT infrastructure included, but expect shorter lease terms and more complex approval processes.

The sublease game works best when you need space quickly and care more about monthly rent than long-term control. Just know you’re trading customization options and lease length for immediate savings.

When Sublease Rents Exceed Direct (Yes, It Happens)

Manhattan’s sublease market gets weird in certain pockets where tenants pay premiums for space someone else already left.

City Hall sublease space averages $53.00 per square foot while direct Class A space runs $47.50 – a $5.50 markup for secondhand space. Chelsea shows an even bigger gap: sublease options hit $89.00 per square foot compared to $74.63 direct. Brooklyn follows the same pattern with sublease at $53.33 versus $47.50 direct.

Why? Aren’t you paying more for someone else’s leftovers?

There are actually several positives to subleasing premium spaces. One is that they usually come turnkey with high-end furniture, custom buildouts, and specialty installations that would cost months and serious money to replicate. Think law firm conference rooms with built-in technology, agency spaces with creative elements, or tech offices with collaborative layouts.

The shorter lease terms also command premiums because some tenants value flexibility over long-term commitments. You get immediate occupancy without construction headaches, but you pay for that convenience.

Before signing any premium sublease deal, though, check the condition and reuse value of existing improvements. Review landlord consent requirements since some buildings make assignment transfers painful. Understand your restoration obligations when the sublease ends and how rent adjustments work if you need to expand or shrink your footprint mid-term.

Sometimes paying extra for plug-and-play makes sense. Just make sure you know what you’re investing money in.

Manhattan Premium vs. Outer Borough Reality

Premium subleases aside, the biggest pricing gap in NYC happens when you cross borough lines – and smart tenants use that geography to their advantage.

That said, while Manhattan’s Class A rents dwarf the outer boroughs across the board, the savings aren’t always as dramatic as you’d expect.

Brooklyn delivers the most Manhattan-like experience at $49.28 per square foot borough-wide with 36.6% vacancy. Downtown Brooklyn pushes into Manhattan territory at $61.44 per square foot, while North Brooklyn stays affordable at $41.05. South Brooklyn splits the difference at $48.02, though sublease options oddly cost more at $53.33.

Queens covers the widest range. Borough average sits at $40.84 per square foot, but submarkets vary wildly. South Queens hits $32.99 while Northeast Queens reaches $52.38 direct – and $65.08 aggregate when trophy buildings enter the mix. Central Queens offers a middle ground at $42.73 with a tight 8.3% vacancy, while South Queens struggles with 52.6% vacancy.

Bronx and Staten Island offer limited Class A inventory. Bronx averages $45.00 with 34.6% vacancy, Staten Island $40.00 with just 13.9% vacancy. Both boroughs require careful building-by-building evaluation since true Class A stock stays thin.

Outer borough plays work best for cost-per-seat optimization, but top-tier locations like Downtown Brooklyn and premium Queens nodes price surprisingly close to Manhattan’s affordable fringe neighborhoods.

The Takeaway: Price Is a Headline, Micro-Market Is the Story

Outer borough savings make sense for some tenants, but Manhattan’s Class A market proves that micro-location beats macro trends every time.

Manhattan’s $63.84 per square foot average means nothing when Grand Central hits $93.37 and Murray Hill trades at $43.21. The spread between direct rents and sublease deals creates even bigger opportunities – especially when Midtown subleases drop to $32.95 while direct space costs $78.60.

Three moves separate smart tenants from everyone else.

First, run parallel searches for both direct and sublease space in your target neighborhoods. Missing sublease inventory costs you negotiating power.

Second, expand your search radius one or two submarkets in every direction, particularly across the Midtown South creative corridor, where a few blocks can save serious money.

Third, target high-vacancy areas like FiDi, Chelsea, and parts of Soho where landlords offer richer tenant improvement packages and longer free rent periods to fill space.

The bottom line is that the right three-block radius matters as much as finding the right building. Get specific with your neighborhood comparisons, and you can land Manhattan prestige at Downtown pricing. Or justify paying trophy rents when address and branding drive your business forward.

Class A office rents in NYC make sense once you stop thinking citywide and start thinking block by block.