Most tenants walk into a Manhattan lease negotiation with the same shrug. “A lease is a lease,” they think. The landlord hands you a commercial lease agreement, a rider gets tacked on, you sign the back page, and get back to running your business.

If only it were that simple in the Manhattan office market.

Don’t believe me? To prove it, I grabbed 10 recent Manhattan office leases off my desk, anonymized them, and lined them up side by side. The comparison points were the ones tenants actually feel in their bank account and their blood pressure: rider length, free rent, tenant improvement dollars or landlord build-out, security deposit, lease term, annual escalations, and whether a Good Guy Guaranty snuck into the package.

By the end of ingesting and analyzing them, I wound up with ten files and zero patterns.

Sure, a couple were tidy standard-form leases with riders hovering around 20 pages. But others were fully customized long-form monsters, 40 to 56 pages of clauses that someone’s attorney clearly earned their fee writing. Same city, same product, same month, and the paperwork looked like it came from different planets.

Why I Pulled 10 Leases Instead of Quoting “Market Norms”

A market report won’t tell you what’s inside the leases it’s averaging. You get an asking rent range, a vacancy number, maybe a chart with an arrow pointing up or down. Useful enough for a board meeting. Useless for a tenant trying to figure out whether their own deal is any good.

The details that actually decide that question, the free rent someone walked away with, the security deposit their landlord held the line on, the clause an attorney dropped on page 34 of the rider, never make it into a survey.

So I went another direction. I analyzed ten recent Manhattan office leases, stripped the identifying details, and compared them side by side:

- A mix of building classes, submarkets, and deal sizes, so I wasn’t looking at one slice of the market

- No addresses, no tenant names, no landlords named, because none of that matters for what I’m trying to show

- The terms that hit tenants in the wallet, not the ones that look good in a brochure

Ten files won’t settle any debates about where the market is headed. What they will do is show you how much the paper can vary from one deal to the next, which is the part tenants never see until they’re deep into their own negotiation.

The two tables below break each deal down by the clauses that quietly drain budgets over the long term. Insurance thresholds. Holdover penalties. How electricity gets charged. Guard fees, emissions surcharges, bulb replacement line items. The structure of the guaranty and when it releases, if it releases at all. These are the clauses tenants stumble onto in year three, usually when accounting flags an invoice and wants to know what it covers.

You’ll see a few cells marked “not surfaced.” The extracted text didn’t expose that term cleanly enough for me to honestly report it, so I left it blank to stay on the safe side.

Table 1: The hidden cost clauses

N/A = clause not present. “Not surfaced” = clause exists but specific terms not cleanly extracted.

| Deal / submarket | Insurance | Electricity | Building fee | Other pass-through | Holdover |

|---|---|---|---|---|---|

| Deal C — Flatiron | $5M umbrella | Charges/taxes passed through | $100/mo guard | CMA charge; bulbs extra | N/A |

| Deal G — Penn District | N/A | Included | N/A | N/A | 150% + add’l rent |

| Deal H — Flatiron / NoMad | N/A | Tenant pays own power | N/A | 12.30% HVAC share | N/A |

| Deal I — Midtown | $5M CGL | Rent inclusion; LL can switch to submeter/direct | ERIF $3.50/RSF | 5% line loss + 15% redistribution + taxes | N/A |

| Deal J — Midtown East | N/A | Article exists; detail not surfaced | $22/mo guard | $22/mo rubbish + 0.78% guard escalation | Article exists; % not surfaced |

Table 2: The exit and liability clauses

N/A = clause not present. “Not surfaced” = clause exists but specific terms not cleanly extracted.

| Deal / submarket | Guaranty type | Release trigger | Early exit | LL relocation | Tail / clawback |

|---|---|---|---|---|---|

| Deal A — FiDi | Full personal | None surfaced | None surfaced | Article exists; detail not surfaced | Survives term; holdover can hit 200% or FMV + new-tenant damages |

| Deal B — SoHo | Guaranty article exists | Not surfaced | None surfaced | None surfaced | N/A |

| Deal D — Penn District | Full guaranty | None surfaced | None surfaced | Yes | N/A |

| Deal E — Meatpacking / West Village | Full | 6-mo vacate notice + clean surrender | None surfaced | None surfaced | Abatement / broker fee / LL work clawback |

| Deal F — Hudson Square | Good Guy | 120-day notice + surrender | None surfaced | None surfaced | Covers holdover / use & occupancy |

Term lengths ran from a little over two years on the short end to well past 10 on the long end. The paperwork varied just as wildly, from loft-style leases short enough to finish on a subway ride to institutional documents that clearly passed through two law firms before they ever hit anyone’s desk.

The First Big Takeaway: The “Standard Lease” Is Mostly a Myth

That paperwork spread is the first real lesson. The “standard lease” most tenants picture walking in is mostly a myth. The landlord’s printed form is an opening bid. The rider is where the economics get rewritten, the risk gets reassigned, and the operating rules get set.

The sample proves it. One deal finalized in late 2024 paired a REBNY form with a 73-article rider. Another came as a custom Washington Street lease with a 40-article table of contents. A Midtown Class A draft ran 56 pages on security, tax escalation, electricity, HVAC, signage, and relocation rights. Another FiDi draft was custom long-form paper, too.

Rider length matters. It tells you how customized the owner’s paper is, how much operational control they want to keep, and how much legal ground a tenant has to cover before touching the economics. Once tenants stop viewing Manhattan office leases as standardized, the rest of the table makes sense.

Free Rent Was All Over the Place, and Not Always in the Way Tenants Expect

Rider length sets the stage. The economics inside the rider tell the real story, and free rent is where that story gets strange fast. Tenants walk in expecting a clean formula, something like five months free on a five-year deal. The sample refused to cooperate.

One tenant got five months free starting at commencement. Another got roughly three months up front before rent kicked in. A third got five months too, but sliced across months 1, 2, 15, 27, and 39. A smaller deal spread its abatement between early-term and later anniversary dates. Others walked away with little or no traditional free rent at all.

Free rent is a structure, not a number. Front-loaded abatement helps move-in cash flow. Staggered abatement bails you out in later years. A deal with no free rent can still beat its peers if the landlord is funding real build-out or easing up on security.

Manhattan office leases rarely follow one blueprint here.

Tenant Improvement Money Mattered Less Than I Expected; Landlord Work Mattered More

Free rent structure tees up the next surprise. Tenants walk in asking about the TI allowance. On smaller and mid-sized Manhattan office leases, the sharper question is what the landlord is really delivering.

The range in this sample told the story. A medical office deal had the landlord building out a lab, a consult room, and a treatment room with plumbing and the electrical to match. Another landlord agreed to modify a prebuilt space, tied commencement to substantial completion, and layered five months of free rent on top. A short West Village lease came largely as-is, with the landlord doing minor work like removing furniture and sealing glass. Another Varick Street deal had the landlord building a conference room instead of writing a check.

A cash allowance sounds cleaner. Landlord work can be worth more if it cuts downtime and construction risk. An as-is deal works too, if the rent concession pencils out.

Security Deposits and Guaranties Told the Real Risk Story

Rent is the number everyone talks about. Deposits and guaranties are how landlords protect themselves when the rent stops coming in, and those two terms moved further across the sample than anything else I pulled.

The deposit spread was wild. One small-office tenant put up a couple of months’ rent and called it a day. A few others landed in the $34,000 to $40,000 zone. A Washington Street deal on a shorter term asked for $67,963, cash or letter of credit, tenant’s choice. A Broome Street landlord wanted $90,000 sitting in their account before anyone turned a key.

Guaranties ran the same gauntlet. Most deals had one. Some were hard personal guaranties with no off-ramp. One ran a clean Good Guy and cut the guarantor loose 60 days after a proper surrender. One deal had no guaranty at all.

Put those two variables next to each other and you can almost see what each landlord thought of the tenant walking in. A $90,000 deposit plus a full personal guaranty reads one way. Two months’ rent and no guaranty reads another. Neither number shows up on a Manhattan office lease term sheet, and both tell you more about the deal than the rent ever will.

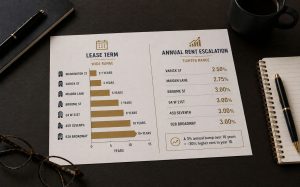

Lease Term and Annual Bumps Were Tighter Than the Other Variables, but Still Not Uniform

Not every term swung as wide as the deposit column. Annual escalations were the quietest part of the whole table.

Most of the deals bumped rent somewhere between 2.5 and 3 percent a year. A Varick Street lease came in at the low end, 2.5 percent flat. Maiden Lane split the difference at 2.75. Broome Street, 54 West 21st, 450 Seventh, and 928 Broadway all sat at or near 3.

No outliers, no surprises, no landlord trying to sneak in a 4 percent bump.

Term length was where things got interesting again. The shortest deal in the sample barely cleared two years. The longest stretched past a decade. That spread drove almost everything else on the page. A short lease tended to come with a fatter deposit or less landlord work. A long lease bought more free rent, more build-out, and room to argue about the guaranty.

Plug a 3 percent annual bump into a 10-year Manhattan office lease, and year 10 rent is roughly 30 percent higher than what you signed for. The escalation clause is the least dramatic line in the rider and quietly one of the most expensive.

What NYC Tenants Should Do With This Information Before Signing a Lease

All of the above means nothing if you walk into your next negotiation still staring at the rent number.

Before the lease goes to your attorney, sit with these questions:

- Am I looking at headline rent or real occupancy cost? Face rent is a starting line. Electric, escalations, tax passthroughs, guard fees, emissions charges, rubbish, bulb replacement. Stack them all, and the number changes quickly.

- What form is the concession in? Five months free, a TI check, and a landlord-delivered build-out are three different animals. They don’t solve the same problems, and they don’t move the same amount of money.

- How much cash does the deposit pull out of the business? Ninety grand in a letter of credit is ninety grand you can’t use for payroll, inventory, or the next hire. That’s real.

- Is the guaranty a real Good Guy, or something heavier? Find the release trigger and read it twice. A 60-day cap after a clean surrender is one world. A personal guaranty that rides the full term is another.

- What’s buried in the rider? Holdover at 200 percent. A relocation clause. Insurance minimums you’ll pay premiums on for a decade. The economics you fought for up front can get quietly undone on page 34.

One rule covers everything else: stop comparing leases term by term. Compare the whole package.

A lease that looks cheap on paper can turn expensive once the landlord refuses to do any work, demands a bigger deposit, and drags the guaranty across the full term. A lease that looks expensive can end up the smarter deal when the landlord delivers usable space, hands over real free rent, and leaves cash in your business instead of parking it in their escrow account.

Winning a Manhattan negotiation is about reading the package, not chasing a headline number. The landlord already knows that. The tenants who catch up are the ones who stop trading.

That’s what the tables above are for.

Nothing Is Standard Except the Word “Negotiable”

Ten files, ten different deals. The only thing they truly had in common was that every term in every lease was up for grabs.

The landlord’s printed lease is a starting position and nothing more. The real deal gets worked out in the rider, or in a custom long-form document an attorney pulled off a shelf and rewrote for the occasion. Walk in asking about the rent, and you’re already losing ground. Ask about the whole structure, and you’re finally in the conversation.

A Manhattan office lease is a risk document, a cash-flow document, and a record of how hard both sides pushed. Holdover, relocation, insurance, indemnification carve-outs. These surface in year three or year seven when something goes wrong, and the lease the tenant signed turns out to be a different lease than the one they thought they signed.

That’s why the attorney matters as much as the broker. The right one reads a lease the way I do, with one eye on legal exposure and the other on the money.