The Safest Manhattan Neighborhoods to Rent Office Space

Crime in Manhattan makes the news more than renting commercial office space nowadays.

Chelsea office space is what you lease when you want loft character and a serious address without paying glass-tower rents. The neighborhood sits inside Midtown South, one of the tightest and priciest office markets in the country right now, running from the West Village up to Hudson Yards with the High Line threaded through the middle of it.

The thing to understand before you start touring is that Chelsea isn’t one market at all. A rebuilt trophy loft on the High Line and a walk-up suite three blocks east off Sixth Avenue can sit on the same map and price a hundred dollars a foot apart, because the neighborhood is really four or five small markets stacked on top of each other. Land in the wrong one and you’ll either overpay or miss the deal that was sitting a block over.

For the money, you get prewar bones, oversized windows, high ceilings, and neighbors that range from Google to the West Chelsea galleries to half the city’s tech and fashion names. That mix is most of the appeal, and it explains why the recovery here has been so real. It simply hasn’t landed evenly, so the value is still there for tenants who know which blocks to walk.

One number won’t tell you where Chelsea is headed, but this will: the loft nobody wanted five years ago is the loft everybody wants now. Across Midtown South, leasing just posted its strongest first quarter since 2019 at 3.0 million square feet, availability tightened to 17.5%, down 380 basis points on the year, and net absorption ran positive at more than 683,000 square feet through the spring (CBRE and Newmark, 2026). Chelsea has been one of the main beneficiaries.

Underneath that sits the wider Manhattan story. The market as a whole tightened to 13.0% availability, its lowest reading since October 2020, and free rent slipped to 12.4 months, the lowest since 2019 (Colliers, Q2 2026). The leverage tenants enjoyed two years ago is draining out of the market, and it is draining fastest from the kind of character space Chelsea is built on.

Anybody who hands you a single number for Chelsea is guessing. The neighborhood runs from side-street Class C in the low $50s all the way up to rebuilt West Chelsea loft well past $100 a foot, and those two buildings might be two blocks apart. So the honest version looks like this: Midtown South, Chelsea’s parent market, averaged $84.77 a foot at 17.5% availability in the most recent read (CBRE, May 2026), while aggregator data puts Chelsea’s own blended asking closer to $96, pulled up by the West Chelsea premium (SquareFoot, 2026).

From there the numbers split by pocket, and the bands in the table below are our own, anchored to that district data, since no approved firm publishes a clean Chelsea-only breakout (Metro Manhattan internal research, July 2026).

Which means the real question was never what Chelsea costs. It is whether your business actually needs a High Line address. Client-facing tech, fashion, and media firms sometimes do, and there is no shame in paying for it, though plenty of strong companies do not, and for them the loft core off Sixth and Seventh is the smarter money nearly every time. Either way, before you tour a single floor, run your headcount through our office space calculator so you are chasing the right amount of space instead of the best-looking lobby.

| Chelsea Pocket | Class A Profile | Class B / C Coverage | Availability | Typical SF (new leases) | Tier |

|---|---|---|---|---|---|

| West Chelsea / High Line (10th & 11th Aves) | Trophy loft, $95 to $150+ | Limited; premium only | ~8 to 12% | 5,000 to 100,000+ | Trophy / A |

| Chelsea Market corridor (Ninth Ave) | Class A, $80 to $110, Google-heavy | Thin | Very tight, ~7 to 11% | 10,000 to 100,000+ | Class A |

| Loft core (23rd to 30th, 6th to 8th) | Repositioned A, $75 to $95 | Deep Class B, $55 to $80 | ~13 to 17% | 2,000 to 30,000 | Mixed / value |

| NoMad / Broadway edge (26th to 30th) | Some Class A | Class B and renovated loft, $55 to $85 | ~14 to 18% | 1,500 to 20,000 | Value / loft |

| Side streets & Meatpacking edge | Limited Class A | Class C and walk-up, $45 to $65 | ~15 to 19% | 500 to 8,000 | Value |

| Midtown South (context) | $84.77 district average | 17.5% availability | 17.5% | Varies | Mixed |

Chelsea pocket bands are Metro Manhattan internal research (July 2026), anchored to Midtown South district figures from CBRE (May 2026) and Newmark (1Q26, April 2026), with a blended-asking reference from SquareFoot (2026). No approved brokerage publishes a clean Chelsea-only average, so treat any single Chelsea number, including ours, as a starting point for touring, not a quote. Rents are asking rents, before concessions.

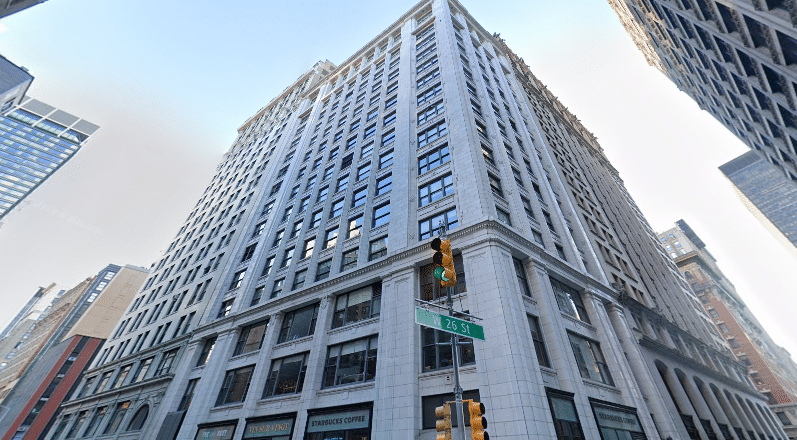

This is the most expensive slice of Chelsea, and it earns the premium. West Chelsea hugs the Hudson from 14th up to 30th, the stretch where old warehouses now share their blocks with Gagosian, Pace, and Hauser and Wirth and the High Line runs past the second-floor windows. More than two hundred galleries give the district its character, and while the space is loft rather than glass tower, it trades at trophy prices.

The marquee addresses are Terminal Warehouse on Eleventh Avenue, the Starrett-Lehigh Building at 601 West 26th, and the IAC Building at 550 West 18th. What tenants are paying for in those buildings is ceiling height, light, big floor plates, and the neighborhood itself, not a letter on a rent roll. So if West Chelsea is where you have to be, plan around timing as much as budget, because the floors worth having tend to move quickly once they reach the market.

Chelsea’s Class A core clusters around Eighth and Ninth Avenues, led by 111 Eighth Avenue, Google’s 2.9-million-square-foot campus, and 75 Ninth Avenue above Chelsea Market, which Google owns as well. The complication is that Google occupies the bulk of it, so while this is genuine prestige inventory, the available space is thin and much of what does come loose arrives as sublease.

When something opens in this pocket it tends to lease quickly and rarely lands cheap. Sitting on top of the A, C, E, and L trains with the Chelsea Market food hall across the street, the buildings mostly sell themselves. For most tenants, though, they are more aspiration than plan, and the real value sits a few blocks east in the loft core.

This is where most Chelsea deals actually get done. The densest run of loft buildings sits between 23rd and 30th from Sixth over to Eighth, with the strongest stock along Seventh Avenue: prewar bones, oversized windows, wood floors, and exposed brick and beam, in buildings like 1133 Broadway, 22 West 19th, and 71 West 23rd.

For years Class B was the automatic value play in Chelsea, but that reputation has aged. Asking rents across Midtown South Class B set record highs in late 2025 (Lee & Associates, Q4 2025), so a good deal here is still very much available; it just tends to hide in the free rent and the improvement money rather than the face rent. A lot of these floors read like true loft space the moment you walk in, which is why the pocket keeps pulling tenants who would otherwise be chasing SoHo lofts at a higher number.

If your priority is keeping fixed costs down and you have no need for a lobby that impresses clients, the side streets are where Chelsea’s real bargains live. Most of the stock is older walk-ups and small mid-block elevator buildings, often with a single exposure and less natural light, but they come with genuine character, high ceilings, and the same wood floors you would pay a premium for a few blocks west.

Nobody publishes a clean Class C average for Chelsea, so treat any single figure you are quoted as a guess (Metro Manhattan internal research, July 2026); in this tier, walking a building tells you far more than an average ever could. It is the right home for solo operators, early-stage startups, and nonprofits that would rather put their money into people than into prestige. If you would rather weigh Chelsea against other loft markets before committing, our rundown of the best NYC neighborhoods for loft-style office space is a sensible place to start.

Concessions are the part of a Chelsea deal where tenants routinely leave money behind, usually because they pour their energy into shaving the asking rent and treat the free rent and the build-out allowance as afterthoughts. Those two line items move the real math far more than the face number does. The market has tightened, so the packages are not as rich as they were a couple of years ago, but outside the Class A trophy floors there is still meaningful room to negotiate.

On a typical five- or ten-year term, recent Chelsea deals have landed roughly here, with shorter terms pulling the concessions down and longer ones pushing them up:

| Building class | Free rent (typical) | TI allowance (typical) | Notes |

|---|---|---|---|

| West Chelsea trophy loft | 8 to 12 months free | $90 to $130/SF | The thinnest package in the neighborhood, but still worth negotiating. |

| Class A / Chelsea Market corridor | 10 to 14 months free | $80 to $120/SF | Prestige space that still comes with some give. |

| Class B loft core | 12 to 18 months free | $55 to $90/SF | Prebuilt suites are common, and a 10-year term is your leverage. |

| Class C and side streets | 12 to 16 months free | $35 to $60/SF | Usually already built out and ready to move into. |

Concession ranges are typical-market figures from Metro Manhattan broker data (July 2026), and they vary by credit, term, and building. For reference, Manhattan's H1 2026 average free-rent period fell to 12.4 months and average TI allowance was about $140/SF (Colliers, Q2 2026).

Two habits will save you real money at this stage. Judge every deal on its effective rent, the figure you actually pay once the free months are spread across the term, because that number almost always sits well below the face rate; our breakdown of rising landlord concessions walks through how the math works. The build-out allowance, meanwhile, is worth only what it pays to construct, so settle who pays for the build-out and lock in a lease term that fits before the real negotiating starts. Our take on the savvy approach to lease clauses covers the rest of what is worth pushing on.

Chelsea has never been a one-industry district, but at heart it is a tech, media, and fashion town with a gallery scene layered over it. Tenants here tend to sort themselves by type rather than scatter, so your clients, your talent, and the firms you partner with are usually already sitting on particular blocks. Line your own industry up against the right pocket and a good chunk of the search sorts itself out, which is what the table below is built to help you do.

| Industry | Best-Fit Chelsea Pocket | Class Fit | Example Buildings |

|---|---|---|---|

| Tech / SaaS / AI | Loft core, West Chelsea | Class A / B loft | 111 Eighth Ave, Starrett-Lehigh, 275 Seventh Ave |

| Media / Advertising / PR | West Chelsea, Sixth Ave edge | Class A / B loft | 675 Sixth Ave (Mattel Bldg), Starrett-Lehigh, Terminal Warehouse |

| Fashion / Design / Showrooms | West Chelsea, Chelsea Market | Premium loft | 601 West 26th, 75 Ninth Ave, 550 West 18th |

| Art Galleries / Creative | West Chelsea (10th & 11th Aves) | Loft / ground floor | 210 Eleventh Ave, West 20s gallery blocks |

| Healthcare / Medical | Sixth & Seventh Aves, side streets | Class B / C | 675 Sixth Ave, side-street loft |

| Prof. Services / Finance | NoMad / Broadway edge, Seventh Ave | Class B loft | 1133 Broadway, 1140 Broadway, 71 West 23rd |

| Startups / Small Biz (<20) | Loft core, side streets | Class B / C | 22 West 19th, 11 West 19th, 54 West 21st |

Industry and class fits are Metro Manhattan internal research (July 2026). Vertical landing pages: Startup & Tech Space, Financial Services, Law Firm Offices, Medical Offices, Retail / Stores. Building and industry examples reflect publicly reported tenancy and recent leases; illustrative, not exhaustive.

A couple of things the table cannot quite capture are worth saying out loud. A startup or small tech team hunting for office space gets the most for its money in the loft core off Sixth and Seventh, the same pocket that earns Chelsea a place on our shortlist of the best Manhattan neighborhoods for small businesses. If you have outgrown a coworking desk and are eyeing your first real lease, our guide to moving from coworking to your own office covers that particular jump. Should the lower rents of the Financial District ever start to look better than trophy loft, that is a genuinely fair trade, and one worth pricing out before you decide.

If your last real tour of Chelsea was before 2020, the version in your memory is out of date. Amenities here have caught up with Midtown’s trophy towers, and in West Chelsea they have gone past them, because the way landlords compete now is on the experience of actually coming in to work. What you can expect falls into three broad tiers.

Chelsea’s retail and showroom frontage along the avenues is some of the most-walked in the city, so retail and store space here moves on its own logic. See all Chelsea buildings or filter active listings by size and price.

Before you tour, it helps to know who actually owns Chelsea, and the short version is that Google is not just the neighborhood’s biggest tenant but one of its biggest landlords, holding 111 Eighth Avenue, Chelsea Market, and 450 West 15th Street outright. Past that, ownership runs to a mix of loft specialists and institutional players, and no two of them come to the table quite the same way. Working out which owner will fund a build-out and which will hold the line on the last dollar is the kind of detail that quietly decides how good your deal turns out, and it is most of what a broker who knows these blocks is actually being paid for. Our rundown of the biggest commercial real estate landlords in NYC maps the wider field.

| Landlord | Notable Chelsea Properties | Approx. Footprint | Typical Lease Profile |

|---|---|---|---|

| Google (owner-occupier) | 111 Eighth Ave, 75 Ninth Ave (Chelsea Market), 450 West 15th St | ~4M SF (owns and occupies) | Owns and occupies |

| RXR Realty | 601 West 26th Street (Starrett-Lehigh) | ~2.3M SF (single asset) | 5,000+ SF loft floors |

| L&L Holding Co. | Terminal Warehouse (261 Eleventh Avenue) | ~1.2M SF (redeveloped) | 10,000+ SF |

| IAC / InterActiveCorp | 550 West 18th Street (IAC Building) | Owner-occupied HQ | Owner-occupier |

Portfolio figures are approximate and limited to Chelsea and adjacent holdings (Metro Manhattan internal research, July 2026). Beyond these owners, much of West Chelsea's loft stock sits with private and boutique landlords rather than large REITs, which is part of why deal terms vary so much block to block. Ownership and management change, so confirm at lease time.

Roughly 50-plus Chelsea offices are on the market right now, from sub-1,000 SF suites to full loft floors.

Transit is one of the genuine reasons to sign a lease on these blocks. Chelsea is among the best-connected pockets on the West Side: the Sixth, Seventh, and Eighth Avenue lines all run straight through it, the L handles the 14th Street crosstown, and the 7 reaches Hudson Yards at the northern edge. For most teams that adds up to a one-seat ride from large parts of Brooklyn, Queens, and New Jersey. Rather than let commute times turn into a running argument once everyone is on board, it is worth checking real home addresses against our commute calculator before you commit.

| From | To Chelsea (23rd St) | Mode |

|---|---|---|

| Hoboken, NJ | 15 to 20 min | PATH to 23rd Street |

| Jersey City (Exchange Place) | 15 to 25 min | PATH to 23rd Street |

| Williamsburg, Brooklyn | 15 to 25 min | L to Sixth or Eighth Avenue |

| Downtown Brooklyn | 20 to 30 min | 2 or 3 to 23rd Street |

| Long Island City, Queens | 20 to 30 min | 7 to Hudson Yards, then a short walk |

| Grand Central (Midtown) | 12 to 18 min | 6 to 14th Street, then L crosstown |

| Newark, NJ | 25 to 35 min | PATH to 23rd Street |

Chelsea runs a wide range, from side-street Class C in the low $50s per foot to rebuilt West Chelsea loft well past $100. As a benchmark, its parent market, Midtown South, averaged $84.77/SF in the most recent read (CBRE, May 2026), and aggregator data puts Chelsea’s blended average near $96/SF (SquareFoot, 2026). Your number depends on the pocket, the building, and the build-out.

West Chelsea, along the High Line between 14th and 30th, packs rebuilt loft icons, 200-plus art galleries, and Hudson River frontage into a few blocks. The space is loft, not glass tower, but ceiling height, light, floor plates, and the neighborhood push rents into trophy range. Rebuilt buildings like Terminal Warehouse and Starrett-Lehigh anchor the top of the market.

Usually, yes, outside the West Chelsea trophy fringe. Hudson Yards on Chelsea’s northern edge is new trophy tower space at the very top of the market, while most of Chelsea is loft that prices below it. You give up the glass-tower finishes, but you keep loft character and the same trains, and the loft core off Sixth and Seventh runs well under the trophy number.

It’s a tech, media, and fashion district first, with a gallery scene on top. Tech and AI firms, advertising and PR shops, fashion and design houses, and art galleries lead, alongside healthcare and professional-services tenants on the loft floors. 2026 leasing drew names like Hightouch, Candid Health, Wave Sports, and Populous to Chelsea and its borders.

Chelsea moves with Midtown South, which sat at 17.5% availability in the most recent read, down 380 basis points year over year (CBRE, May 2026). Manhattan overall fell to 13.0% in Q2 2026, its lowest since 2020 (Colliers, Q2 2026). Premium loft and the Chelsea Market corridor are far tighter than the headline number suggests.

Small tenants usually find the best value in the Class B and Class C loft core off Sixth and Seventh Avenues, in buildings like 22 West 19th, 54 West 21st, and 11 West 19th. Many landlords now offer prebuilt spec suites with furniture and cabling so you can move in fast, often on flexible three- to five-year terms.

Google is the giant, occupying its 2.9-million-SF campus at 111 Eighth Avenue and owning Chelsea Market across the street. The Starrett-Lehigh Building, owned by RXR, houses Ralph Lauren, Tommy Hilfiger, and Under Armour, among others. L&L Holding redeveloped Terminal Warehouse, and IAC owns and occupies its building at 550 West 18th.

Still meaningful, but shrinking. Manhattan free rent averaged 12.4 months in the first half of 2026, the lowest since 2019, with TI allowances near $140/SF (Colliers, Q2 2026). On a Class B Chelsea loft you can typically negotiate a few months of free rent plus a solid TI package, especially on a longer term. The effective-rent math is where the real savings hide.

In a loft market like Chelsea, the letter grade bends. A rebuilt 1930s warehouse can technically be Class B and still out-rent a Class A tower, because tenants pay for light, ceiling height, and location, not the grade. Class A here means the Chelsea Market corridor and rebuilt West Chelsea icons; Class B is the loft core; Class C is the side-street walk-ups.

It depends on your stage and budget. Both are loft markets with a creative pull, so the call often comes down to price and vibe. SoHo leans fashion and design-forward retail with cast-iron lofts, while Chelsea gives you the Google halo, the gallery scene, and a wider spread from value to premium. Chelsea’s edge is range: you can start cheap in the loft core and scale up toward the High Line without leaving the neighborhood.

Accessibility Tools