Here’s a number that should snap you out of whatever you think you know about the NYC office market: 401 buildings are completely full right now. That’s 64.7 million square feet of space you can’t lease, and over half of it sits outside Midtown.

I pulled the CoStar data myself because I didn’t believe it either. SoHo, Tribeca, Chelsea: submarkets where tenants thought they’d score deals are pushing rents up while everyone obsesses over misleading vacancy stats. The good space got absorbed fast.

SL Green filling 919 Third Avenue to 100% occupancy after the state grabbed more floors is just one example of what’s happening across Manhattan. Leasing volumes blew past pre-pandemic levels. Vacancy rates started dropping. And the three-year tenant’s market officially ended.

Manhattan’s Leasing Rebound: Record-High Activity

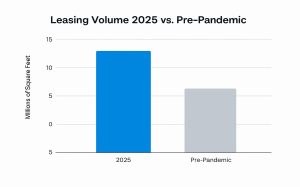

Those 401 fully leased buildings I mentioned are just the tip of the iceberg. Manhattan tenants signed more leases in the first nine months of 2025 than in any comparable period since before the pandemic, and the velocity keeps accelerating. We’re watching years of pent-up decisions finally hit the NYC office market all at once.

The Numbers Tell You Everything

Manhattan started 2025 with 12.2 million square feet leased in Q1, the strongest quarter since 2019. Q2 added another 8.4 million square feet (also the highest since 2019), and Q3 kept the momentum with 7.3 million square feet.

Do the math: we’re running 20 to 30 percent ahead of last year’s pace, with new and renewal activity up nearly 40 percent.

The deals themselves got bigger, too. NYU grabbed 1.1 million square feet. Multiple law firms renewed six-figure footprints. The mega-lease came back from the dead.

Finance and Tech Are Writing the Checks

Bloomberg just renewed and expanded to 925,000 square feet at 919 Third Avenue. Financial services firms account for almost 37 percent of major leases signed in the first half of 2025. Tech companies that went remote in 2020 are quietly taking floors again, and media firms are consolidating into better spaces rather than shrinking.

Class A buildings are absorbing most of this demand, yet the 401 fully leased buildings span every class type. You’ve got 31 Class A towers completely full, but also 54 Class B buildings and 21 Class C properties with zero availability. Quality wins first, but everything decent follows.

The Inventory Reality Nobody Wants to Admit

Here’s what the CoStar data reveals about those 401 buildings: the average size is 161,000 square feet, with asking rents hovering around $56 per square foot based on range midpoints.

You want specifics? 120 Park Avenue in Midtown: 643,000 square feet, fully leased. 915 Broadway in Gramercy: 250,000 square feet, gone. 260 Spring Street in Hudson Square: 281,000 square feet, not available.

Even Staten Island got tight. 1441 South Avenue has 391,000 square feet completely absorbed. When Staten Island office buildings fill up, you know Manhattan’s market fundamentally changed. The space you could negotiate on last year became the space you lost out on last month, and the pattern keeps repeating across every submarket that matters.

Vacancies and Availabilities are Finally Falling

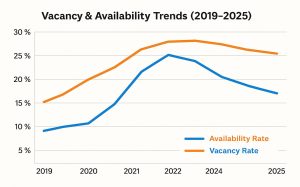

All that leasing velocity had to eat into something, and now we’re watching the inventory problem fix itself in real time. Manhattan vacancy just hit 22 percent, down from nearly 30 percent last year, and the good space is disappearing way faster than the overall numbers suggest.

The Numbers Are Moving Fast

Three years of elevated vacancy trained everyone to expect unlimited options. That era just ended. Manhattan’s vacancy rate dropped to 22 percent in Q3, the lowest since early 2023, while sublease space shrank for the fifth straight quarter. Direct vacant space stabilized around 77 million square feet, and for the first time since 2020, tenants absorbed more space than hit the market.

Net absorption went positive in Q3. You know what that means? More square footage got leased than became available. The market physics reversed, and many tenants haven’t caught on yet.

Good Luck Finding What You Actually Want

Total Manhattan availability dropped from 20 percent to 17.7 percent year-over-year, which sounds like plenty of options until you look at what tenants actually want. Midtown Class A availability sits under 12 percent. Central Midtown? 7.5 percent.

The 401 fully leased buildings tell you exactly what’s working. The median one was built in 1931 but renovated in 2011. Prewar bones with modern systems are crushing glass boxes from the ’80s, and landlords who upgraded their lobbies and elevators during COVID now get to choose their tenants. The power flipped faster than anyone expected.

The Great Space Shuffle Created a Shortage

Every tenant who upgraded to a better space in 2023 and 2024 removed two options from the NYC office market: the premium space they took and the decent space they left behind, which immediately got absorbed. Now the chain reaction is complete. Trophy buildings filled first, Class A followed, and suddenly, even Class B buildings in good locations have waitlists.

The kicker? Older buildings keep getting converted to residential, pulling more inventory offline permanently. Meanwhile, new construction barely exists. So while your spreadsheet shows 22 percent vacancy, your requirement for decent light, functional layout, and working elevators leaves you with maybe three real options. And two of them could be gone by next week.

Neighborhood Hotspots and Size Niches Are Tight

The vacancy drop varies depending on where you’re looking and how much space you need. Some neighborhoods barely have anything left, and if you’re hunting for that perfect 15,000-square-foot floor in Midtown South, you might want to sit down for this.

The Geography of Full Buildings Tells the Story

Those 401 fully leased buildings spread across the city in revealing patterns. Midtown has 27, Midtown South has 25, but here’s what should grab you: Queens has 19, Brooklyn has 16, and Staten Island has 7 completely full buildings. Over half the fully leased inventory sits outside traditional Midtown.

SoHo, Hudson Square, Tribeca, Chelsea, and Gramercy Park lead the pack for creative and tech tenants. Take 260 Spring Street in Hudson Square: 281,000 square feet, completely absorbed. The media and tech companies that migrated to these neighborhoods during the last cycle locked down the best buildings, and they’re not giving them back.

Tribeca’s overall vacancy runs just 16 percent, way below Manhattan’s average. The Flatiron and NoMad districts are even tighter. SoHo looks available on paper until you realize most of that vacancy sits in aging loft buildings.

The Mid-Size Space Squeeze Nobody Saw Coming

While everyone focused on million-square-foot deals making headlines, the real shortage developed in the 5,000 to 20,000 square foot range. Try finding a decent 15,000-square-foot block in core Midtown South right now. You can’t.

The 20,000 to 40,000 square foot segment got equally challenging. Companies that need a whole floor in a boutique building are discovering that those buildings are full. Well-lit, open-plan spaces in this size range generate multiple offers within days of hitting the market. Tenants looking to expand within Flatiron, Union Square, or the West Village are getting priced out of their own neighborhoods.

Even Brooklyn and Queens Got Expensive

Brooklyn’s 16 fully leased buildings and Queens’ 19 tell you something important: Manhattan tenants aren’t the only ones feeling squeezed in the NYC office market. Williamsburg’s creative lofts spark bidding wars. Long Island City’s newer buildings filled up while Manhattan-focused brokers weren’t paying attention.

Small creative firms that saw Brooklyn as their affordability escape hatch are learning that the window’s closed. The same boutique floors that used to sit empty for months in Dumbo or Gowanus now get three offers in the first week. Landlords in these markets spent years jealous of Manhattan rents, and now they’re catching up fast.

Yes, the outer borough discount still exists. However, it’s shrinking every quarter, and the good spaces disappear just as quickly as Manhattan inventory.

What’s Driving Demand – Why Tenants Are Flocking Back

So how did we go from empty towers to bidding wars in three years? The answer involves a mix of corporate conditions, expiring leases, and the simple fact that Zoom calls can’t replace everything. Tenants stopped debating whether to come back and started fighting over the best spaces to return to.

The Anchors Locked Down the Best Buildings First

Those 401 fully leased buildings didn’t fill up with small tenants. Corporate and government anchors grabbed multiple floors or entire buildings, locking that inventory for the next decade. When the state takes more space at 919 Third or a bank claims half a building, that space never hits the open market.

Smart landlords also learned to play defense. They’re reshuffling tenants internally, expanding one company from three floors to five while consolidating another from two floors to one. The building stays full, the tenants get what they need, and you never see a listing. The vacancy that should exist simply doesn’t.

Finance and Tech Stopped Pretending Remote Works

Wall Street and Big Law are forcing people back four or five days a week. BlackRock took 290,000 square feet at 50 Hudson Yards. Salesforce renewed 314,000 square feet at 1095 Avenue of the Americas. The banks and hedge funds that tried remote work in 2021 discovered junior bankers can’t learn the job from their apartments.

Tech companies, especially the AI and data firms, need their teams together to build products. Venture-backed startups realized they can’t compete for talent without a real office. The sector that pioneered remote work is quietly taking floors again, and they want good buildings with outdoor space and natural light.

Everyone Figured Out Their Hybrid Formula

The endless hybrid debate finally ended. Companies know whether they need people in person for three days or four days or every day, and they’re signing leases based on real patterns instead of wishful thinking. No more “we’ll take less space and hot-desk it.” Teams that need collaboration are back with defined schedules.

Creative firms split the difference with a flagship location in Midtown and smaller spaces downtown. Media companies consolidated from three mediocre locations into one great building. The operational chaos of 2020 to 2023 gave way to clarity, and clarity means signing leases.

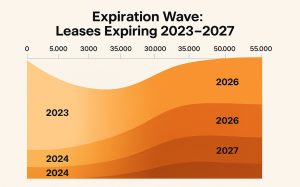

The 2026-2027 Expiration Wave Started Early

55 million square feet of leases expire through 2027; tenants impacted are renewing now because they see what’s happening to availability. Wait until 2026 to negotiate? Good luck finding options in this NYC office market.

Landlords know this timeline, too. They’re offering early renewals to lock in tenants before the market gets worse (for tenants). The rates are higher than the last lease. Yet, tenants are signing anyway because the alternative is entering a market with 401 buildings already off the table.

NYC Employment Quietly Hit Records

NYC private sector employment just hit a new high. Companies are hiring, teams are growing, and all those people need desks. The stabilized job market turned theoretical space needs into actual lease signings.

Media, design, and fashion firms are back in growth mode. Consultancies are staffing up. Even retailers are taking office space again. The latent demand that built up during three years of uncertainty is hitting the market simultaneously, and there’s not enough quality space to absorb it all. The tenants who recognize this reality are signing now.

Pricing and Strategy: How Tenants Should Play the New Scarcity

All this demand hitting a tight NYC office market means one thing: the playbook you used in 2023 is dead. The average asking rent across those 401 fully leased buildings runs about $56 per square foot, but that number becomes meaningless when you can’t find space at any price. Here’s how to work the market that actually exists, not the one you remember.

- Start Looking Six Months Before You Think You Need To: The days of touring twelve options for your 15,000-square-foot requirement are over. If you need space in Midtown South for next year, start looking now, because three of your five options will disappear before you finish your second round of tours.

- Forget Perfect and Focus on Functional: That dream floor with perfect light and ideal layout? Someone else signed for it last week. Target ready-to-occupy spaces even if they’re 80 percent of what you want, because waiting for perfection means paying 20 percent more for a worse space six months from now.

- Trade Tenant Improvements for Speed: Landlords know you’re in a hurry, and they’re not. If you need to move fast, offer to take less TI money in exchange for lower rent or faster occupancy. A built-out floor you can occupy next month beats raw space that won’t be ready until summer.

- Lock In Your Fallback Options Early: Identify two backup spaces in nearby submarkets and stay engaged with those landlords. Put down soft holds where you can. The perfect space you’re chasing might never hit the market, and your Plan B from January becomes someone else’s Plan A by March.

- Use Your Renewal as Leverage While You Still Can: If your lease expires within the next two years, your landlord wants to keep you because they see what’s happening to vacancy rates. Negotiate your renewal now while you still have some leverage, because next year you’ll be competing with everyone else whose lease is expiring, and the conversation will be very different.

The NYC Office Market Window Is Closing Fast

Those 401 fully leased buildings aren’t coming back to the market. Vacancy dropped and keeps falling, leasing volumes hit multi-year highs, and even neighborhoods you wrote off are getting competitive.

You want to wait for better deals? They’re not coming. Every week you delay means fewer options and higher rents. Because the market already flipped.

Stay informed, act decisively, and work with local experts – because week after week, the tower lobbies will be a little emptier, and the waiting lists a little longer.