Zohran Mamdani, a 34‑year‑old state assemblyman, Muslim, and self-described democratic socialist, just became NYC’s mayor after defeating former governor Andrew Cuomo with just over 50% of the vote, ending a political dynasty and making history as the youngest mayor since 1890.

Wall Street’s watching. So are landlords, developers, and every tenant wondering if their rent might actually stop climbing. Mamdani campaigned on rent freezes, city-run grocery stores, free buses, and taxing the wealthy — policies that sound great at rallies but send shivers through boardrooms across Manhattan.

Commercial real estate faces its biggest ideological shift since rent control. Everything from office towers to retail spaces to development projects gets reassessed when the mayor-elect calls capitalism the problem, not the solution. Some investors have already started recalculating property values. Others see opportunity where competitors see crisis.

So what’s the truth about Mamdani’s impact on real estate? How unprecedented is this really? Does it really mean cheaper office space for startups or a mass exodus?

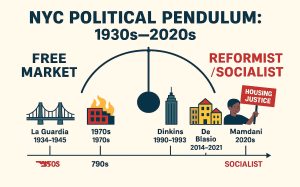

Historical Context: When Politics Moved the Market

New York real estate has always danced to City Hall’s tune. Every generation gets its reformer promising to fix the housing mess, and every generation watches the market convulse, adapt, and somehow keep spinning. Mamdani’s victory feels revolutionary, but NYC has played this game before. The city swings between free-market fever dreams and socialist experiments like a pendulum powered by voter rage. This isn’t our first rodeo.

La Guardia Built the Blueprint (1934-1945)

Fiorello La Guardia rode FDR’s New Deal wave straight into City Hall and turned federal cash into concrete. He constructed bridges, tunnels, schools, and public housing projects that physically remade Manhattan and the boroughs. Most importantly for today’s market, he birthed modern rent control in 1943 when wartime price freezes became permanent fixtures. That emergency measure evolved into today’s rent regulation system—now covering about a million apartments, though most are under the newer “rent stabilization” rules rather than the original rent control. Either way, La Guardia proved mayors could fundamentally alter how housing works with alterations that stick around longer than anyone expects.

The 1970s Showed What Happens When Cities Break

New York was a disaster in the 1970s, when President Ford famously told the bankrupt city to drop dead (or close enough). Crime exploded, landlords torched their own buildings for insurance money, and the South Bronx became a synonym for urban decay. Rent-controlled buildings sat empty because owners couldn’t profit from them. The crisis then forced the city to loosen regulations and court developers again. Lessons were learned: push too hard against market forces and watch the market abandon you entirely. Pull back and watch it return, cautiously, with demands.

Dinkins Tried First (1990-1993)

David Dinkins already tested the democratic socialist mayor experiment three decades before Mamdani. He pushed community policing, housing equity, and hate crime laws. Local real estate interests and NYC-focused REITs panicked then, too—though the broader market barely noticed. But recession and budget cuts hamstrung his agenda before it could transform much. Giuliani swept him out after one term, bringing broken-windows policing and developer-friendly policies. Dinkins proved progressive mayors could win in NYC. He also proved that winning and governing require different skills entirely.

De Blasio’s Recent Progressive Push (2014-2021)

Bill de Blasio campaigned on his “tale of two cities” and actually delivered some wins. Universal pre-K happened. The Rent Guidelines Board approved its smallest increase ever (1%) in 2015. He launched plans for 300,000 affordable units, though only about 110,000 materialized. He wanted wealth taxes and stock transfer taxes, but Albany blocked them. Homelessness hit record highs despite the efforts. De Blasio showed progressive policies could pass, but market forces move faster than government programs. Affordability remained a crisis even with an interventionist mayor pulling every lever available.

Chicago and San Francisco Wrote the Cautionary Tales

Other cities tried their own experiments. Chicago banned rent control statewide, then tried inclusionary zoning instead. Twenty years later, they’d built fewer than 3,000 affordable units while overall construction lagged. San Francisco went the opposite direction, covering 70% of apartments with rent control while strangling new supply with zoning. Result: the most expensive housing in America and a “zoning tax” adding $400,000 per home. Both cities now frantically reverse course, trying to build their way out of crises their own policies helped create.

NYC’s property market has survived a lot. Each era left marks: rent control from the ’40s, abandonment scars from the ’70s, gentrification from the Giuliani years, and affordability mandates from de Blasio. Mamdani represents the next swing of that pendulum, armed with bigger promises than any predecessor. History says he’ll change some things permanently, fail at others spectacularly, and leave the next mayor to clean up whatever remains.

Tax, Transit & Tenants: Mamdani’s Agenda in Focus

History shows NYC mayors can reshape real estate markets. Now, Mamdani gets his turn with the boldest toolkit yet. His platform reads like a progressive wish list accumulated over decades of watching other cities fail and succeed, with Mamdani’s impact on real estate as bold as it is uncertain when you break down his actual policy plans:

- Corporate Tax Hike: Mamdani wants NYC’s corporate tax rate to jump from 7.25% to 11.5% (matching New Jersey’s), plus a 2% wealth surcharge on millionaire incomes. That’s $9-10 billion yearly in new revenue. Companies already paying Manhattan rents now face Manhattan taxes to match. Some will eat the cost, others will look for an exit.

- Rent Freeze on 1-2 Million Apartments: Every rent-stabilized unit gets frozen immediately for four years under Mamdani’s plan. Landlords who budgeted for standard increases just watched their spreadsheets explode. Tenants finally catch a break after years of racing against rising rents. The math gets ugly fast for building owners counting on steady revenue growth.

- City Grocery Stores and Free Buses: Mamdani wants NYC to run supermarkets selling at wholesale prices, one per borough, minimum. All buses go fare-free too, costing $800 million annually. Government competing with bodegas and Key Food while eliminating MetroCard swipes sounds wild, but stranger things have worked elsewhere.

- Office-to-Housing Conversions Get Pushed: Mamdani backs aggressive office-to-housing conversion incentives. The 467-m program offers 90% tax breaks for 35 years if developers convert offices to apartments. But the problem is, 25% must be rent-stabilized, and his rent freeze makes those units less appealing to create.

- Mayor’s Office to Protect Tenants: Forget calling 311 about broken heat. Mamdani’s plan includes creating an enforcement office with teeth, tripling violation fines, and giving tenants direct mayoral backing against negligent landlords. Building owners who skated on repairs before a better budget for maintenance or lawyer fees.

These policies hit every corner of commercial real estate, whether you own, rent, lease, or invest. Office landlords face higher taxes and pressure to convert. Residential owners lose rent growth while enforcement tightens. Retail spaces compete with city-run stores. Developers must factor in new costs, new rules, and new risks., The question becomes whether NYC’s market adapts like it always has, or whether this time the pendulum swings too far.

Early Market Reaction

Stocks that are heavily influenced by NYC events heard Mamdani’s victory speech and immediately freaked out. REITs dropped, developers froze, and private equity firms started whispering about “distressed opportunities.” Without being biased, the market’s response tells you a lot about Mamdani’s impact on real estate before he’s even taken office. Money moves faster than policy, and right now it’s moving cautiously, sideways, or straight into wait-and-see mode.

REITs Take the First Hit

NYC-focused real estate investment trusts felt the pain immediately. Empire State Realty Trust, Vornado, and SL Green all dropped between 1%-5% on election night, with some sliding further the next morning. Flagstar Financial, heavily exposed to rent-stabilized buildings, saw investors bail even faster. These weren’t panic sells but calculated retreats. Portfolio managers who watched Vornado drop 6.7% after Mamdani’s June primary victory knew what came next. REITs generate returns through rent growth and property appreciation. Mamdani’s platform attacks both. Institutional investors don’t wait around to see if campaign promises become law; they price in the risk and move on.

Developers Hit Pause on Everything

Many developers and lenders stopped signing checks the morning after election night, and are now firmly in “wait-and-see” mode. Nobody wants to buy a building today using yesterday’s financial models when tomorrow’s regulations could wreck the math. Small landlords face worse prospects. A rent freeze on aging buildings without revenue growth means deferred maintenance becomes permanent. Banks are already nervous about commercial lending at 7% interest rates, and now they have to add political risk to their spreadsheets.

Private Money Circles Like Sharks

Family offices and private equity funds adopted classic disaster capitalism positioning. They’re sitting on capital, watching, waiting for someone to blink first. These players know distressed assets emerge when policy shifts collide with overleveraged owners. They’ve seen this movie before during COVID, 2008, and the 1970s. They’re building relationships with nervous landlords, studying which buildings might flip from profitable to problematic under new rules, and keeping powder dry for the moment someone needs to sell fast.

REBNY tried calming nerves, pledging “constructive engagement” with the new administration. Luxury brokers insist exodus talks are overblown. Yet the concerns are there and aren’t going anywhere anytime soon.

Where the Money Goes Next: Sectors and Capital in Motion

Market reactions tell you what happened yesterday. Sector analysis tells you what happens tomorrow. NYC commercial real estate splits into distinct ecosystems, each processing Mamdani’s impact on real estate differently. Office towers, retail strips, and investment funds all face unique calculations. Some sectors might thrive under socialist policies while others suffocate. The smart money studies which is which.

Office Space: Convert or Die?

Manhattan offices face brutal math: 22% vacancy in Midtown, companies wanting half the space they used to lease, and now a mayor who thinks corporate taxes should double. Yet 2025 saw the most office leasing activity since 2006, with 23 million square feet signed. JPMorgan and Amazon still want Manhattan addresses.

The contradiction resolves through conversion. NYC leads nationally with 4.1 million square feet of offices becoming apartments. The 467-m program offers 90% tax breaks for conversions, though Mamdani’s rent freeze complicates the required 25% affordable units. Tech startups and AI firms increasingly choose flexible coworking spaces (up 8% in outer boroughs) over traditional leases.

Everyone, though, fears the San Francisco scenario: taxes and regulations so oppressive that companies discover Austin has both sunshine and spreadsheets that work. Whether NYC avoids that fate depends on how many offices transform into housing before their owners give up entirely.

Retail Real Estate Splits in Two

Mamdani loves bodegas and hates chains, and his policies reflect it. John Catsimatidis, who owns Gristedes supermarkets, already announced he’s selling 25% of his NYC properties after calling Mamdani’s election “bad for business.” Other national retailers might follow.

Yet neighborhood shops see opportunity. City-run grocery stores competing on price could anchor commercial strips. Local businesses benefit from customers with frozen rents having more disposable income. Fifth Avenue and Times Square lose their appeal when corporate taxes spike and regulatory scrutiny intensifies. But Astoria, Bed-Stuy, and Jackson Heights gain when policies favor independents over franchises.

Retail real estate becomes hyperlocal: your strip mall in Queens might thrive while Madison Avenue struggles. Landlords who bet on community retail over luxury flagships could win big.

Capital Finds New Paths

Institutional money hates uncertainty more than bad news.

REITs and pension funds pulled back from NYC deals, waiting for policy dust to settle. Some redirect toward suburban properties or sunbelt markets where math stays predictable. Family offices see opportunity where institutions see risk. They’re studying which overleveraged owners crack first under frozen rents and higher taxes. Distressed assets create fortunes for buyers with patience and capital. Due diligence costs spike when every deal needs triple the legal review, but that same complexity keeps amateur investors out.

The smartest players recognize patterns from previous cycles: capital flees, values drop, brave money returns, fortunes get made. NYC survived the 1970s bankruptcy, 9-11, 2008 crisis, and COVID. Mamdani’s socialism might scare institutional investors today, but tomorrow someone buys their abandoned positions at discounts that make the risk worthwhile.

Potential Winners and Losers

Every political earthquake creates new fortunes while crushing old ones. Mamdani’s impact on real estate aims to redistribute wealth as much as his tax plans, and the market has already started sorting itself into camps: those who profit from progressive policies and those who pay for them. Your position depends entirely on what you own, where you own it, and who pays your rent.

Winners

Outer-borough landlords just caught a break. Mixed-use buildings in Queens and Brooklyn with ground-floor bodegas and apartments above suddenly look brilliant. These properties generate steady cash from resilient neighborhood retail and residential rents that won’t crater like Manhattan office towers might.

Affordable housing developers also hit the jackpot with Mamdani’s promised $100 billion funding surge. They’ll build while others freeze, collect subsidies while others pay taxes, and face streamlined approvals while luxury developers fight new regulations.

Coworking operators like WeWork’s successors can also barely contain their excitement. Companies ditching 50,000-square-foot leases need somewhere to land, and flexible workspace grew 8% in outer boroughs alone last year. Community retail landlords benefit when Gristedes leaves and local grocers move in, especially if those city-run supermarkets actually materialize to anchor neighborhoods.

Social impact funds and tenant advocacy groups finally get a mayor who speaks their language and writes policies for their portfolios.

Losers

Trophy office owners could watch their empires wobble. SL Green and Vornado already dropped 5-7% and that’s before any actual policies take effect. They own the gleaming Midtown towers that companies increasingly abandon for cheaper, flexible alternatives.

Luxury condo developers face an even darker reality: their buyers hate taxes more than they love Central Park views. When millionaires pay 2% wealth surcharges, penthouses become harder sells.

Rent-stabilized portfolio owners could also feel pain. A four-year rent freeze on properties that already operate on thin margins means choosing between maintenance and mortgage payments. Many won’t get to choose. Corporate tenants and national chains pay twice: higher taxes on their profits and higher costs for their locations. Catsimatidis already started selling. Others will follow.

Wall Street landlords who leveraged up during COVID, counting on rent growth, just learned that math works both ways.

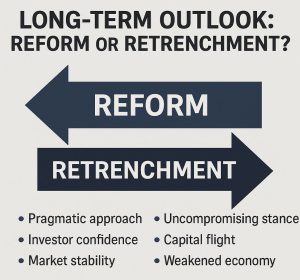

Long-Term Outlook: Reform or Retrenchment?

Winners and losers emerge quickly, but NYC’s real estate market plays the long game. Mamdani faces the same choice every revolutionary mayor confronts: compromise to survive or fight until something breaks. His first 100 days will signal which path he picks. Albany watches, developers wait, and tenants hope. The market needs answers about whether Mamdani’s impact on real estate stays rhetorical or becomes structural. Here’s what determines if NYC gets reformed or wrecked.

- The Pragmatic Path vs. The Purist Play: Mamdani either moderates his proposals to keep investors engaged or doubles down on socialist principles regardless of market reaction. Smart money bets on pragmatism once reality hits. Public-private partnerships for housing, phased tax increases, and infrastructure investments could balance his equity goals with market stability.

- Albany Holds the Cards: Governor Hochul already called tax hikes a “non-starter,” and she controls what reaches Mamdani’s desk. The state legislature loves NYC’s tax revenue but hates scaring away the companies that generate it. Real estate lobbyists own more Albany phone numbers than Mamdani has supporters, and they know how to use them.

- Budget Math Beats Campaign Math: NYC faces multi-billion dollar deficits without chasing away a single taxpayer. Every company that leaves, every wealthy resident who relocates, makes those holes deeper. Mamdani needs their money to fund his programs. That cruel irony forces even socialist mayors to keep capitalists happy enough to stay and pay.

- The City Council Reality Check: Council members from Queens and Brooklyn want affordable housing but also want development in their districts. They’ll support tenant protections but balk at killing construction jobs. Mamdani needs their votes for zoning changes and tax abatements, giving them leverage to dilute his boldest plans.

- Performance Determines Persistence: Markets forgive ideology if results follow. Deliver actual affordable housing, improve transit, reduce crime, and investors return despite higher taxes. Fail to execute while raising costs, and watch capital flee to Miami and Austin permanently. Mamdani gets maybe two years to show progress before patience expires and money moves.

The Bottom Line for Your Office Space

NYC survived bankruptcy, 9/11, Hurricane Sandy, and COVID. Mamdani’s socialism ranks somewhere below those on the catastrophe scale. The city adapts because it has to, and so will you, whether you’re a landlord or tenant.

Your next moves matter more than Mamdani’s campaign promises. Tenants should lock in favorable terms before policies are clarified and leverage returns to landlords. Owners need flexibility built into new leases while tracking which tax proposals actually survive Albany. Watch City Council votes, not mayoral speeches. Track actual legislation, not Twitter speculation.

Markets hate uncertainty more than bad policy. Right now, everyone’s swimming in both. Metro Manhattan Office Space knows these waters and is here for you, no matter what your concerns are. So, reach out. We’ll help you answer any questions you have.