How Loss Factor Impacts Commercial Space

You make an appointment to see a New York City commercial space that, judging from some online photos, is ideal for your business.

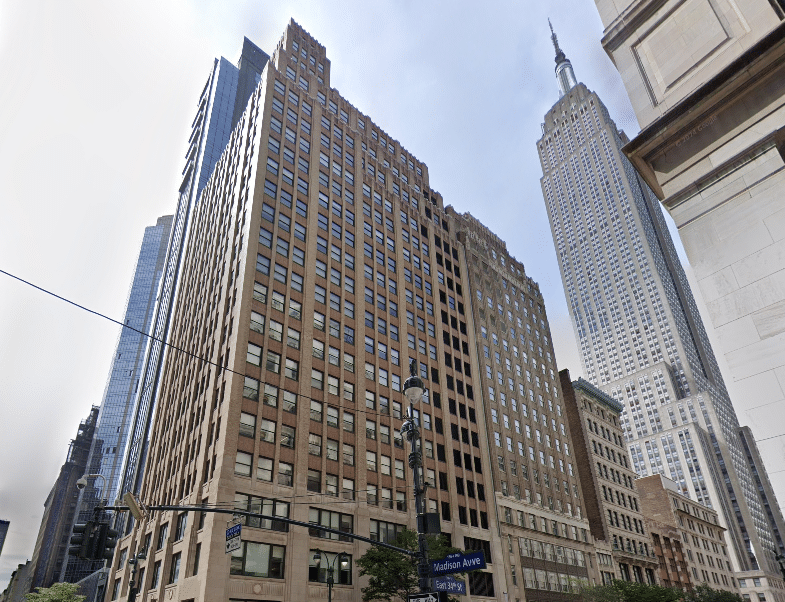

Murray Hill sits just below and east of Grand Central, a pocket of brownstones, walk-ups, and prewar office buildings that stayed quiet while the rest of Midtown got louder and more expensive. The Empire State Building marks one corner; the East River is a few blocks the other way. What you get here is a Midtown address minutes from Grand Central, priced well below most of the district.

Asking rents average about $72.14/SF across the submarket (Avison Young, Q1 2026), below Midtown’s $78.23/SF and a fair bit under the $85.28/SF that Class A commands district-wide (Cushman & Wakefield, April 2026). That average is misleading on its own, since the Class A towers on Park Avenue pull it up. The prewar buildings on Madison and the side streets toward the river run closer to $45 to $65 (Metro Manhattan internal research, May 2026).

Murray Hill also has the most available space of any major Midtown submarket, around 22.4% (Avison Young, Q1 2026). With the rest of Midtown tight, that extra room works in a tenant’s favor: more to choose from, and landlords with a reason to deal. To see what’s open right now, browse Murray Hill office space.

Murray Hill has long been Midtown‘s affordable corner. It kept the prewar buildings and the residential quiet that most of the district traded away, and its rents never climbed the way they did around Grand Central or over toward Fifth Avenue. For a tenant, that adds up to a Midtown address next to the city’s busiest transit hub, at a discount to nearly everything around it.

The wider market is working in your favor, too. Manhattan tenants leased 11.78 million SF in the first quarter of 2026, the busiest first quarter since 2014, and availability fell to 13.7%, down for the eighth quarter running (Colliers, Q1 2026). Midtown asking rents reached $78.23/SF overall and $85.28/SF for Class A (Cushman & Wakefield, April 2026), and CBRE’s May reading had the Midtown average at $84.77/SF and still rising (CBRE, May 2026). Murray Hill belongs to that same tightening market, but its rents haven’t caught up. That lag is what makes it worth a look.

There are really two prices in Murray Hill. The one you’ll see quoted is the submarket average, about $72.14/SF in direct asking rent (Avison Young, Q1 2026), which already runs under Midtown’s $78.23/SF and well under the $85.28/SF Class A average (Cushman & Wakefield, April 2026). That’s reasonable for a Midtown address this close to Grand Central.

The other price is what most tenants actually pay. The Park Avenue towers pull that average up; move a block west to Madison or east toward the river and the prewar buildings often run $45 to $65/SF (Metro Manhattan internal research, May 2026). Two buildings on the same block can quote very different rents, so it pays to tour widely rather than anchor on a single number. Before you start, our Office Space Calculator will help you pin down how much space you actually need.

| Area | Class A Profile | Class B / C Coverage | Availability | Typical SF for New Leases | Tier |

|---|---|---|---|---|---|

| Park Avenue corridor (32nd to 41st) | Prime and renovated Class A (One Park, 100 Park) | Limited | ~12 to 18% | 3,000 to 50,000+ SF | Class A |

| Madison Avenue corridor (30th to 40th) | Some renovated Class A (180, 183 Madison) | Deep Class B and value inventory | ~18 to 24% | 1,500 to 25,000 SF | Class A / B |

| Fifth Avenue and NoMad edge (30th to 34th) | Class A on lower Fifth (Empire State Building) | Class B and showroom space | ~15 to 22% | 2,000 to 30,000 SF | Class A / B |

| Lexington to Third, medical East Side | Some medical Class A | Class B and C, medical and general | ~15 to 22% | 1,000 to 20,000 SF | Class A / B / C |

| Grand Central edge (40th to 42nd) | Class A feeding the terminal (100 Park, 300 E 42nd) | Class B available | ~12 to 18% | 3,000 to 40,000 SF | Class A / B |

| Murray Hill average (context) | $72.14/SF direct asking | n/a | 22.4% total | Varies | Mixed |

Murray Hill direct asking rent ($72.14/SF FS) and total availability (22.4%) from Avison Young Market Intelligence and CoStar (Q1 2026). Area-level profiles, Class B and C coverage descriptors, and availability ranges are Metro Manhattan internal research (May 2026); approved firms publish the Midtown submarket figures but do not publish per-area Murray Hill breakouts. Rents are asking rents and do not reflect concessions.

Class A in Murray Hill mostly means Park Avenue. One Park Avenue, Vornado’s 943,000 SF tower at 32nd Street, leads the group: NYU Langone holds it down on a lease through 2050, and it recently came through a roughly $395 million renovation (Vornado). Heading up the avenue you’ll find 100 Park Avenue (SL Green, at 40th near Grand Central), 2 Park Avenue (the 1928 Art Deco landmark Haddad Brands bought in 2024), and 3 Park Avenue (Cohen Brothers, with a Pelli Clarke Pelli redesign). None of these are trophy buildings in the Plaza District mold, but they’re well-run, well-located, and priced below the Midtown Class A average.

If you’re weighing what actually separates a trophy tower from standard Class A, our piece on how trophy buildings set themselves apart explains the difference, and our roundup of the top Class A buildings in Midtown shows where Murray Hill’s Park Avenue stock fits in.

Most leasing in Murray Hill happens in Class B, and so does most of the value. Madison Avenue and the side streets are lined with prewar towers, some renovated with new lobbies and move-in-ready suites, others left largely as they were. A well-kept Class B floor here can feel like Class A in a pricier neighborhood, for a lot less. 180 Madison and 183 Madison sit at the renovated end of the range, with plainer buildings below them.

Rents sit well under the $72 average, and how far under depends on the building and the block (Metro Manhattan internal research, May 2026). Two Class B towers a block apart can quote very different numbers on the same day, shaped by how much space the landlord is sitting on and how he reads your company’s credit. It’s worth seeing several before you decide what counts as a normal rent.

The lowest rents are in the older, un-renovated buildings, many of them on the side streets and toward the East River, along with the smaller medical and general-office space east of Park. These work well for small practices, back-office teams, and nonprofits, anyone who wants the Midtown location without the full Midtown rent.

One caveat at this end of the market: no firm publishes a reliable Class C average for Murray Hill, so treat any single quoted figure with some skepticism. The read here is Metro Manhattan internal research (May 2026). If you want the full breakdown of how the classes differ, our explainer on what makes a building Class A, B, or C covers it.

Concessions are where tenants tend to under-negotiate. They focus on the asking rent, shave a few dollars, and sign, without pressing on free rent or the build-out allowance, which is often where the bigger savings are. With availability at 22.4%, the highest in Midtown (Avison Young, Q1 2026), there’s more room to push here than almost anywhere in the district, particularly in the Madison Avenue and side-street buildings.

The ranges below reflect typical recent deals on a 5 or 10-year term (Metro Manhattan internal research, May 2026); shorter terms tend to get less, longer terms more. If you’re unsure how long to commit, our comparison of 3-year, 5-year, and 10-year lease terms walks through the trade-offs.

| Building class | Free rent (typical) | TI allowance (typical) | Notes |

|---|---|---|---|

| Renovated Class A (Park Avenue, upper Madison) | 12 to 16 months free | $80 to $120/SF | The smallest concessions in the submarket, though still meaningful. |

| Class B (Madison, side streets) | 14 to 20 months free | $55 to $90/SF | This is where the give is most generous, move-in-ready suites are common, and a 10-year term carries real weight. |

| Class C and value | 12 to 18 months free | $35 to $65/SF | Less finish, but the lowest face rents in Midtown and plenty of negotiating room. |

| Medical | Highly variable | Highly variable | Medical build-outs are costly and specialized, so a landlord chasing a creditworthy practice will often put in more to win a long lease. |

The ranges below reflect typical recent deals on a 5 or 10-year term (Metro Manhattan internal research, May 2026); shorter terms tend to get less, longer terms more. Concession ranges vary materially by landlord, tenant credit, lease term, and building.

Murray Hill’s tenant mix looks different from the rest of Midtown. Healthcare leads, with practices clustered around NYU Langone east of Park. Alongside them are nonprofits and associations on Madison, fashion and showroom tenants on the Fifth Avenue edge near NoMad, finance and law firms in the Park Avenue towers, and a growing number of small and midsize companies that left Midtown South for lower rent. Find your industry in the table below to narrow things down quickly.

| Industry | Best-Fit Areas | Class Fit | Example Buildings |

|---|---|---|---|

| Healthcare / Medical Offices | Medical East Side, Park Avenue | Class A / B / C | One Park Avenue (NYU Langone), 240 E 38th, 333 E 38th, 317 E 34th |

| Nonprofits / Associations | Madison Avenue, Park Avenue | Class A / B | 180 Madison, 3 Park Avenue, Madison prewar stock |

| Financial Services / Asset Management | Park Avenue, Grand Central edge | Class A | One Park Avenue, 100 Park Avenue, 2 Park Avenue |

| Law Firms (boutique and midsize) | Park Avenue, Grand Central edge | Class A / B | 100 Park Avenue, 3 Park Avenue, 300 E 42nd |

| Professional Services / Consulting | Madison Avenue, Park Avenue | Class A / B | 180 Madison, 100 Park, 3 Park |

| Fashion / Showroom / Design | Fifth Avenue and NoMad edge | Class A / B | Empire State Building (350 Fifth), 315 Fifth, 347 Fifth |

| Technology / SaaS / Creative | Madison Avenue, Fifth Avenue edge | Class B | 183 Madison, 185 Madison, Madison side streets |

| Beauty / Wellness | Park Avenue, Madison Avenue | Class A / B | One Park Avenue (Clarins, Equinox), Madison stock |

| Startups / Small Business (under 20 people) | Madison Avenue, side streets | Class B / C | 171 Madison, 136 Madison, value side streets |

| Coworking / Flex | Madison Avenue, Park Avenue | Class A / B | Madison Avenue flex space, Park Avenue suites |

| Retail / Showroom | Fifth Avenue, Madison Avenue | Ground-floor | Empire State Building base, Madison and Fifth frontage |

Industry and class fits are Metro Manhattan internal research (May 2026).

For a small team or a newer practice, Murray Hill is one of the easier Midtown addresses to afford. Between the value buildings on Madison and the side streets and that 22.4% availability, a Midtown location costs less than the district’s reputation would suggest. If you’re comparing neighborhoods, our guide to the best NYC neighborhoods for small businesses lines them up, and if you’re moving out of a shared workspace, here’s how to think about scaling from coworking to your own office. One exception: if you specifically want exposed brick and timber loft space, that’s really a Midtown South search, so start in Chelsea or SoHo instead.

Murray Hill isn’t competing with the Plaza District on amenities, and it doesn’t try to. Its strengths are location and value: a Midtown address next to Grand Central, the Empire State Building on its edge, and prewar buildings with light and detail that newer towers can’t really replicate. The Park Avenue Class A buildings have the updated systems and renovated lobbies; the Madison and side-street buildings trade some of that polish for a lower rent. The space falls into three tiers:

Renovated Class A (One Park Avenue, 100 Park Avenue, 180 Madison): updated lobbies and systems, efficient floor plates, and easy transit. One Park is a LEED Silver tower largely leased to its medical anchor. This is the top of the submarket.

Class B and value (183 Madison, 171 Madison, and the wider Madison and side-street stock): prewar construction, tall windows, attended lobbies, and a growing supply of move-in-ready suites, usually a short walk from Grand Central and the 6 train.

Medical and specialized (the East 38th and East 34th Street cluster): purpose-built and converted medical space tied to NYU Langone, from ambulatory care to orthopedics, on the streets running east toward Kips Bay.

Implementation note: link each building name above to its Metro Manhattan building profile where one exists.

Browse all Midtown buildings, or filter the active listings by size and price.

Who owns a building can matter as much as which building you pick, since each Murray Hill landlord operates differently. Vornado owns One Park Avenue outright and runs it around its medical tenant. SL Green, the largest office landlord in the city, holds 100 Park. Cohen Brothers treats 3 Park as a flagship. Empire State Realty Trust runs the Empire State Building on the Fifth Avenue edge, and the Clarett Group (with PGIM) and Haddad Brands hold renovated Class A space on Madison and Park. Most of the negotiating room, though, is with the many smaller private owners who control the prewar value stock on Madison and the side streets. A broker who works the area will already know which owners fund build-outs and which dig in. For more on the major players, see our piece on the biggest commercial real estate landlords in NYC.

| Landlord | Notable Murray Hill Properties | Approx. Portfolio | Typical Lease Profile |

|---|---|---|---|

| Vornado Realty Trust | One Park Avenue | ~943K SF here; large Midtown portfolio | Class A, 5,000+ SF, medical and office |

| SL Green Realty | 100 Park Avenue | part of SL Green's ~25M+ SF (NYC's largest office landlord) | Class A, 5,000+ SF |

| Cohen Brothers Realty | 3 Park Avenue | ~625K SF here; larger nationally | Class B, 5,000+ SF |

| Empire State Realty Trust | Empire State Building (350 Fifth) | part of ESRT's ~7.8M SF Manhattan portfolio | Class A, 2,000+ SF |

| The Clarett Group (with PGIM Real Estate) | 180 Madison Avenue | ~280K SF here | Class A, 3,000+ SF |

| Haddad Brands | 2 Park Avenue | ~1M SF (single asset, owner-occupier) | Owner-occupier, limited availability |

| Private prewar owners | Madison Avenue and side-street value stock | varies | Class B / C, 1,000+ SF, most negotiable |

Portfolio figures are approximate. Several landlords listed (Vornado, SL Green, Empire State Realty Trust) hold much larger portfolios across Midtown, Midtown South, and Downtown. Metro Manhattan internal research (May 2026).

On transit, Murray Hill is hard to beat, mostly because Grand Central sits right on its northern edge. Staff coming in on Metro-North or the LIRR land a short walk away, thanks to Grand Central and the Grand Central Madison terminal. For subway riders, the 6 runs straight through the neighborhood, and the 4, 5, 7, and S all stop at the terminal. To compare actual door-to-door times, plug your team’s home addresses into our Commute Calculator.

| From | To Murray Hill | Mode |

|---|---|---|

| Grand Central (on-site) | 0 to 5 min | Walk |

| Times Square / Midtown core | 5 to 10 min | 7, S, or walk |

| Upper East Side (86th St) | 10 to 15 min | 4, 5, or 6 |

| Downtown Brooklyn | 25 to 35 min | 4 or 5 |

| Long Island City, Queens | 10 to 15 min | 7 from Grand Central |

| Hoboken / Jersey City | 20 to 30 min | PATH to 33rd |

| Newark, NJ | 30 to 40 min | PATH or NJ Transit to Penn + subway |

| Hicksville, NY (Long Island) | 45 to 55 min | LIRR to Grand Central Madison |

| Stamford, CT | 50 to 60 min | Metro-North to Grand Central |

The submarket average is about $72.14/SF in direct asking rent (Avison Young, Q1 2026), which is below Midtown’s $78.23/SF and its $85.28/SF Class A average (Cushman & Wakefield, April 2026). The Park Avenue towers pull that average up, though. On Madison and the side streets, value space often runs $45 to $65/SF (Metro Manhattan internal research, May 2026), so what you pay comes down largely to the block.

It has always been Midtown’s quieter, more residential corner, and its rents never climbed the way they did around Grand Central or Fifth Avenue. It also has the most available space of any major Midtown submarket, about 22.4% (Avison Young, Q1 2026), which keeps pricing soft and gives tenants room to negotiate. The savings show up most clearly in the prewar Class B and value buildings off Park Avenue.

About 22.4% as of Q1 2026, split between roughly 20.9% direct space and 1.5% sublease (Avison Young, Q1 2026). That’s the highest of any major Midtown submarket, even with Manhattan-wide availability down to 13.7% (Colliers, Q1 2026). Most of the open space is in the older Madison Avenue and side-street buildings rather than the Park Avenue Class A towers.

It’s one of the strongest medical-office submarkets in Manhattan, anchored by NYU Langone. One Park Avenue is roughly 67% leased to NYU Langone through 2050 (Vornado, 2021), and the streets east toward Kips Bay, including 240 and 333 East 38th and 317 East 34th, hold ambulatory care, orthopedic, and medical-arts space. Practices that want to be close to the hospital and its referral network tend to land here.

Increasingly, yes. With Flatiron, NoMad, Chelsea, and Union Square running short on loft space, some tenants are moving into Murray Hill for a cheaper address that’s still close by (Metro Manhattan internal research, May 2026). You give up the exposed brick and timber for more conventional prewar offices, but you pick up Grand Central access and a lower rent. If the loft look is a must, Midtown South is still the place to look.

Usually not on rent alone. Murray Hill’s direct asking rent of about $72.14/SF is below the Midtown average but above the cheapest Manhattan submarkets. For the lowest possible Class A rent, Downtown Manhattan and the Financial District generally come in lower. What Murray Hill offers in return is the Midtown location and Grand Central right there.

Madison Avenue and the side streets are the place to look, where smaller prewar buildings like 171 Madison and 136 Madison offer compact, lower-cost floor plates (Metro Manhattan internal research, May 2026). The high availability means more options and more negotiating room than a busier neighborhood would give a small tenant. Many of these companies would pay noticeably more for the same footprint in Midtown South.

Class roughly reflects a building’s age, systems, and prestige. In Murray Hill, Class A means the Park Avenue towers and a few renovated Madison buildings, while Class B and C cover the older prewar stock along Madison and the side streets. A well-renovated Class B floor here can stand up to Class A in another neighborhood, at a lower rent.

The main owners are Vornado (One Park Avenue), SL Green (100 Park Avenue), Cohen Brothers Realty (3 Park Avenue), Empire State Realty Trust (the Empire State Building), the Clarett Group with PGIM (180 Madison), and Haddad Brands (2 Park Avenue), along with many smaller private owners holding the value stock on Madison and the side streets (Metro Manhattan internal research, May 2026). The largest occupier is NYU Langone, which leases about 67% of One Park Avenue through 2050 (Vornado, 2021).

Grand Central sits on the northern edge, with Metro-North, the LIRR through Grand Central Madison, and the 4, 5, 6, 7, and S trains. The 6 local runs through the middle of the neighborhood at 33rd Street, and the B, D, F, M, N, Q, R, and W stop a few blocks west at 34th Street-Herald Square. Few office addresses in the city are better connected, which is a real part of what you’re paying for.

Much of the best value in Murray Hill, especially in the privately owned prewar buildings, never makes it onto the public listing sites, and a broker can get you in front of those spaces and tell you which owners are negotiating. The landlord pays the commission, so for a tenant it costs effectively nothing. Before you start touring, it’s worth reading the essentials to ask before leasing NYC office space and getting familiar with the Good Guy Guarantee most NYC landlords ask smaller tenants to sign.

Accessibility Tools