Coworking Vs. Traditional Office Space – Which is Right for You?

Finding the right office space is a vital component of your company’s long-term success.

The Plaza District is the most expensive office market in New York. It covers Park Avenue’s Hedge Fund Alley, the Fifth Avenue flagships, the Seagram Building, and the GM Building with the Apple cube in front of it. At the end of March its average asking rent was $94.53/SF, which put it just ahead of Chelsea as the priciest submarket in the city (Yardi, Q1 2026). Companies pay that number for the address.

There is a second figure that matters more than the headline. Regular Class A asks around $73.97/SF direct. Once the trophy towers are included, the aggregate climbs to $103.14/SF (Metro Manhattan, August 2025), and the best Park and Fifth floors run higher than that. The submarket is really two markets sharing the same blocks: a trophy tier that is almost fully leased, and a much larger Class A and B market beneath it where most tenants actually sign. Work out which one applies to you before you start touring.

The trophy tier has almost no space left. Midtown’s prime vacancy is down to 2.9% (CBRE, Q1 2026), and the supply of trophy space has not grown in a single quarter since early 2023 (Newmark, Q4 2025). For a top Park Avenue floor, the limit is availability rather than budget: you take what comes back or you wait for the next one. To see what is listed at the moment, start with Plaza District office space.

The Plaza District has been the top of the Manhattan office market for decades, and the gap is widening. It has the trophy buildings on Park and Fifth, a Central Park frontage, and the largest concentration of finance and law tenants in the city, while very little new space ever frees up. That is what makes it both the most expensive submarket and the hardest one to get into at the high end.

The wider market is strong, which works against tenants here. Manhattan leased 11.78 million SF in the first quarter of 2026, its best opening quarter since 2014, and availability dropped to 13.7% (Colliers, Q1 2026). Midtown accounted for about two-thirds of that, with asking rents of $78.23/SF overall and $85.28/SF for Class A (Cushman & Wakefield, April 2026); CBRE’s May figure was $84.77/SF and rising (CBRE, May 2026). The Plaza District leads all of it. What separates it is the address and the shortage of good available space.

Two numbers describe the Plaza District, and they are far apart. Standard Class A asks about $73.97/SF direct. With the trophy towers included, the aggregate is $103.14/SF (Metro Manhattan, August 2025). Transwestern put the Class A average at $92.01/SF in the fourth quarter of 2025, and the top Park and Fifth trophy floors run from $150/SF into the $200s. That is the widest internal range of any Midtown submarket, so a single average rent for the area is not very useful.

What you pay depends on three things: the corridor, the building class, and whether you need a trophy address or simply a good one. Before touring, run your headcount through our Office Space Calculator so you are looking at the right size range.

| Corridor | Class A Profile | Class B / C Coverage | Availability | Typical SF for New Leases | Tier |

|---|---|---|---|---|---|

| Park Avenue (high 40s to 59th) | Trophy and prime Class A (270 Park, 375 Park, 425 Park) | Very limited | ~7 to 11% | 5,000 to 100,000+ SF | Trophy / A |

| Fifth Avenue & 57th Street | Trophy and prime Class A (GM Building, 9 West 57th, 660 Fifth) | Limited; some renovated Class B | ~9 to 13% | 3,000 to 75,000 SF | Trophy / A |

| Madison Avenue | Renovated Class A (590 Madison, 550 Madison) | Boutique Class B | ~11 to 15% | 2,000 to 30,000 SF | Class A / B |

| Third Avenue & Lexington | Older Class A (Lipstick Building, 919 Third) | Deep Class B; some Class C | ~13 to 18% | 1,500 to 40,000 SF | Class A / B / value |

| Plaza District average (context) | $73.97 Class A direct ($103.14 aggregate); $92.01 Class A (Transwestern) | n/a | 10.4% | Varies | Mixed |

Plaza District Class A direct ($73.97/SF) and aggregate ($103.14/SF) from Metro Manhattan, Class A Office Rents in New York City by Neighborhood (as of August 1, 2025). Submarket availability (10.4%) and Class A average ($92.01/SF) from Transwestern, Q4 2025. Corridor-level Class A profiles, Class B and C coverage descriptors, and availability ranges are Metro Manhattan internal research (May 2026); approved firms publish the Midtown and Plaza District submarket figures but do not publish per-corridor breakouts. Rents are asking rents and do not reflect concessions.

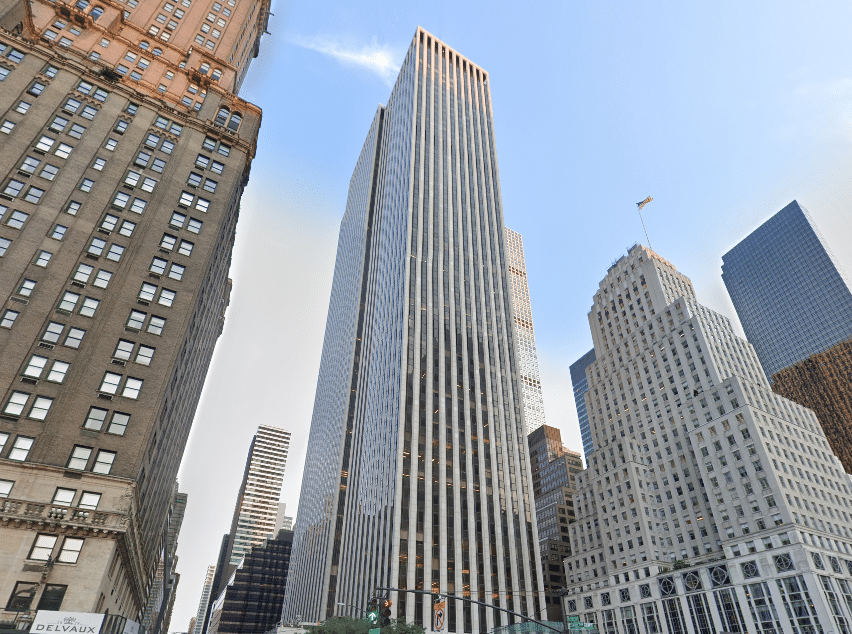

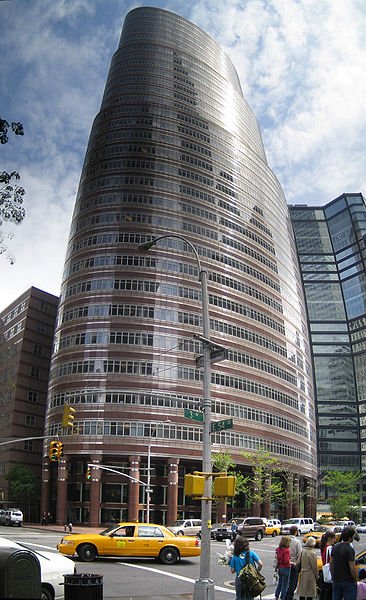

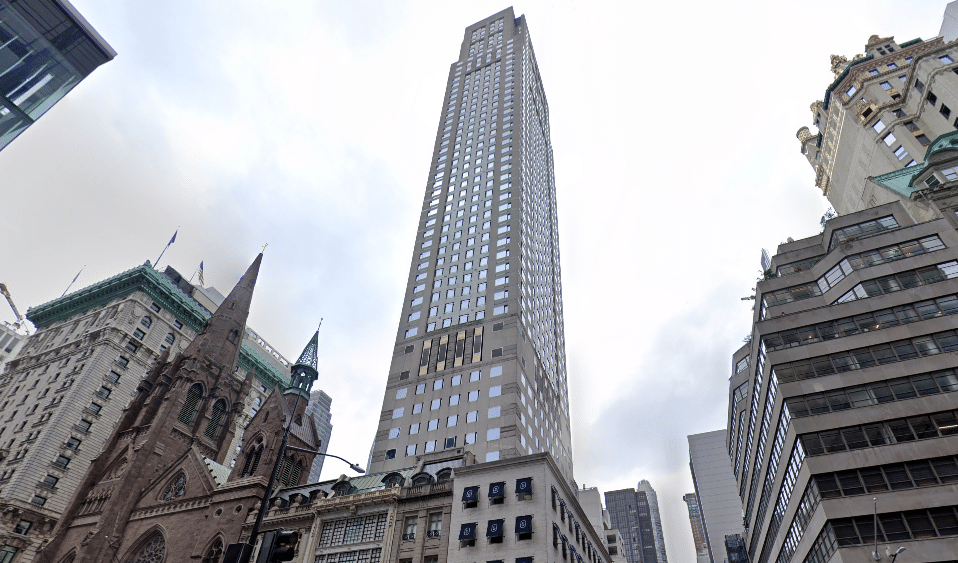

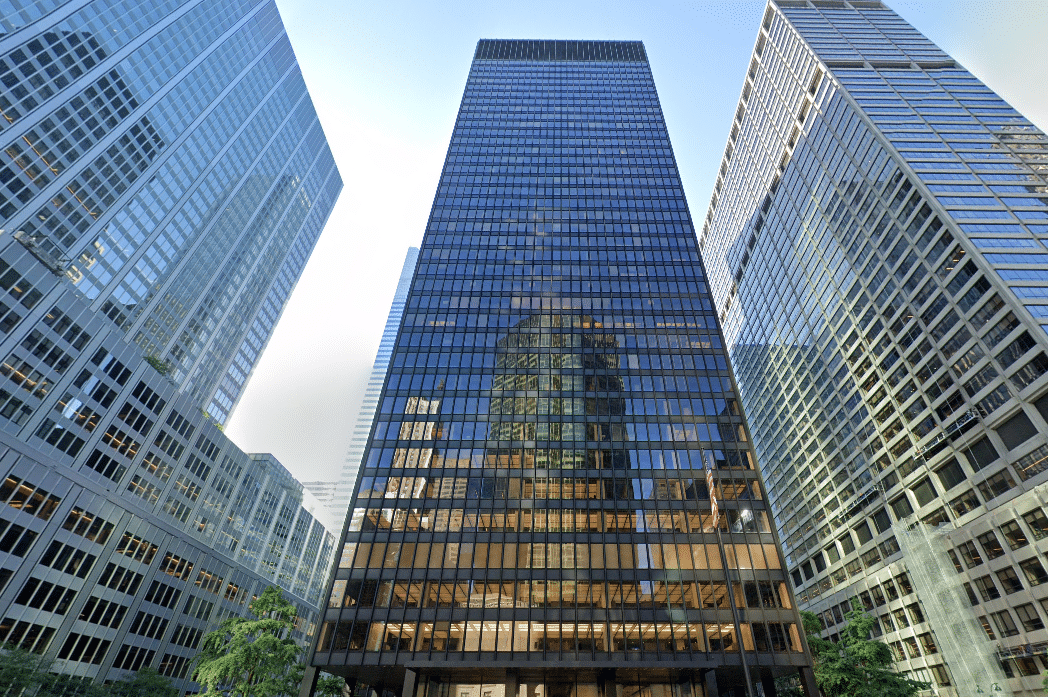

Trophy in this submarket means Park Avenue and Fifth. JPMorgan’s 270 Park set a new high and 350 Park will raise it again, but neither is available to lease. The trophy space a tenant can actually pursue is in buildings like 9 West 57th (the Solow Building, 1.5 million SF with the best park views in Midtown and a longtime hedge fund and private equity address), the GM Building at 767 Fifth (the limestone tower with the Apple cube in front), 425 Park (L&L’s Foster-designed tower, where Citadel holds the penthouse), and the Seagram Building at 375 Park (the Mies van der Rohe landmark). These floors start around $150/SF, they draw several tenants whenever one opens, and the owners screen carefully on credit.

For the difference between a true trophy tower and a strong Class A building, see our piece on how trophy buildings set themselves apart in NYC, and our top Class A buildings in Midtown for the specific addresses.

Most deals in the Plaza District happen outside the trophy towers, a block or two off Park, in the renovated Class A and Class B buildings: the Madison Avenue boutiques, the prewar towers on the side streets, and the larger floors to the east. A good Class B floor here, with an updated lobby, newer elevators, and a built-out suite ready to occupy, would qualify as Class A in much of the city, and the Plaza District address comes at a meaningful discount to the trophy rents.

Pricing falls below the $92/SF Class A average, and how far below depends on the building and the block (Metro Manhattan internal research, May 2026). Two Class B towers on the same block can quote very different numbers on the same day, depending on the landlord’s vacancy and how he reads your credit, so it pays to tour rather than rely on the average. These buildings suit financial services firms, law firms, and medical and healthcare practices, among many others.

There is not much true Class C in the Plaza District; the land is too valuable for buildings to sit unimproved. The closest thing to value is the eastern edge along Third and Lexington, in older boutique buildings and second-tier space that work for small firms, startups, nonprofits, and satellite offices that want the location at a lower rent.

Two cautions. No firm publishes a reliable Class C average for the Plaza District, so treat any single figure with skepticism (the tier read here is Metro Manhattan internal research, May 2026). Tenants who want character space, exposed brick, timber, and large windows, will not find much of it here; that search belongs in Midtown South, usually starting in Chelsea or SoHo, where there is far more loft space at lower rents.

Concessions are where most tenants under-negotiate. They push on the asking rent, save a little, and sign without pressing on free rent or the build-out allowance, which is where much of the real value sits. Because the Plaza District is tighter than most of Midtown, concessions run smaller than in Downtown or Midtown South, though they are still meaningful and grow as soon as you move off the trophy floors.

The ranges below reflect recent deals (Metro Manhattan internal research, May 2026) on a 5- or 10-year term; shorter terms earn less and longer terms earn more. If you are still deciding on length, our guide to 3-year, 5-year, or 10-year lease terms works through the tradeoffs.

| Building class | Free rent (typical) | TI allowance (typical) | Notes |

|---|---|---|---|

| Trophy and prime Class A (Park and Fifth) | 6 to 10 months free | $100 to $150/SF | The smallest packages in Midtown, since these landlords face little competition for the space. |

| Standard Class A (Madison, side streets) | 10 to 14 months free | $80 to $120/SF | The best balance, a Plaza District address with real movement on terms. |

| Class B and value (Third and Lexington) | 12 to 18 months free | $60 to $90/SF | Built-out suites are common, and a 10-year term gives a tenant real negotiating room. |

The ranges below reflect recent deals (Metro Manhattan internal research, May 2026) on a 5- or 10-year term; shorter terms earn less and longer terms earn more. Concession ranges vary materially by landlord, tenant credit, lease term, and building.

Two points worth understanding before you sign. The net effective rent almost always comes in well below the face rent (our concessions explainer walks through it), and a build-out allowance is only as useful as what it pays for, so it helps to know who pays for an office build-out in advance.

The Plaza District is built on finance, law, and corporate headquarters, and the building usually signals the tenant. Park Avenue is hedge funds, private equity, and asset managers (Blackstone at 345 Park, Citadel at 425 Park and soon 350 Park). Fifth Avenue holds the headquarters and the luxury brands. Madison leans toward boutique finance, family offices, and fashion. The eastern edge along Third and Lexington draws the more cost-conscious professional, medical, and back-office tenants who want the location at a lower rent (Bloomberg is at 731 Lexington, IBM anchors 590 Madison). The table below maps the common industries to where they tend to land.

| Industry | Best-Fit Corridors | Class Fit | Example Buildings |

|---|---|---|---|

| Hedge Funds / PE / Asset Management | Park Avenue, Fifth Avenue | Trophy / A | 9 West 57th, 425 Park, 345 Park (Blackstone), 280 Park |

| Financial Services / Banks | Park Avenue, Madison, Fifth | Trophy / A | 270 Park (JPMorgan), 399 Park (Citi), 280 Park (Wells Fargo), 660 Fifth |

| Law Firms (large and boutique) | Park Avenue, Fifth Avenue | Trophy / A | 767 Fifth (GM Building), 375 Park (Seagram), 9 West 57th, 425 Park |

| Corporate HQ / Flagship | Fifth Avenue, Park Avenue | Trophy | 767 Fifth, 270 Park, 550 Madison, 590 Madison (IBM) |

| Family Offices / Wealth Management | Madison, Fifth, Park | Class A | 540 to 595 Madison, 510 Madison, Fifth Avenue boutiques |

| Fashion / Luxury / Advertising | Madison, Fifth Avenue | Class A / B | 550 Madison, 575 Madison, the Crown Building (730 Fifth) |

| Professional Services / Consulting | Third & Lexington, Madison | Class A / B | 805 Third, 875 Third, 919 Third |

| Technology / Creative | Madison, Third & Lexington | Class A / B | 731 Lexington (Bloomberg), 885 Third (Lipstick), 919 Third |

| Healthcare / Medical Offices | 57th Street, Third & Lexington | Class A / B | 57 West 57th (Medical Arts), 120 East 56th, 110 East 59th |

| Coworking / Flex | Park Avenue, Fifth, Madison | Class A / B | 57th Street flex, 110 East 59th, Madison Avenue flex |

| Retail / Showroom | Fifth Avenue, Madison, 57th | Ground-floor | GM Building (Apple), Fifth Avenue flagship corridor, the Crown Building |

Industry and class fits are Metro Manhattan internal research (May 2026).

For a small team, the Plaza District is rarely the obvious choice, since it is the most expensive address in the city. The eastern edge and a few boutique Madison buildings are more attainable than the headline rent implies, though, and for a client-facing business the prestige can justify the cost. To compare it against less expensive areas, our 5 top neighborhoods for small businesses guide lays out the options, and a company moving out of shared space can read scaling from coworking to your own office for the transition. Tenants focused on value should look at Downtown Manhattan or the Financial District, where a Class A address costs a fraction of what it does on Park Avenue.

No part of New York has more recognizable office buildings, and the surrounding amenities match. There is Central Park at the north end, the Fifth Avenue flagships and the Billionaires’ Row towers nearby, five-star hotels and restaurants on most blocks, and subway access from several directions. With return-to-office still a priority for landlords, the Plaza District is an easy area to bring a team back to. The buildings fall into three tiers:

Trophy (270 Park, 9 West 57th, the GM Building, 375 Park, 425 Park): column-free floor plates, double-height lobbies, private amenity floors, conference space, fitness centers, restaurants at the base, and park and skyline views. 270 Park is the largest all-electric tower in the city, and the Solow and Seagram buildings are architectural landmarks.

Renovated Class A (550 Madison, 590 Madison, 660 Fifth, 280 Park, Lever House): updated lobbies and systems, amenity floors, ground-floor retail, and transit nearby. 550 Madison reopened with a public garden, and Lever House recently completed a full restoration.

Class B and value (the Lipstick Building, 919 Third, 875 Third, the Madison boutiques): prewar and postwar construction, staffed lobbies, large windows, and a growing number of built-out suites a short walk from Park and Fifth.

Who owns the building matters as much as which building, because each Plaza District landlord negotiates differently. SL Green and Vornado, the two largest office owners in the city, both hold prime Park Avenue space and share ownership of 280 Park. BXP owns the GM Building and 399 Park. RFR holds the Seagram Building; Rudin owns 345 Park and is a partner on 350 Park; L&L developed 425 Park; Tishman Speyer built 270 Park and owns 300 Park; the Soloviev Group owns 9 West 57th; Olayan owns 550 Madison; and Brookfield owns 660 Fifth. A good broker will know which owners fund build-outs and which ones hold firm on terms. Our overview of the biggest commercial real estate landlords in NYC has more background.

| Landlord | Notable Plaza District Properties | Approx. Portfolio | Typical Lease Profile |

|---|---|---|---|

| SL Green Realty | 280 Park Avenue (JV), 919 Third Avenue, 750 Third Avenue | ~25M+ SF (NYC's largest office landlord) | Class A, 5,000+ SF, 10+ yr |

| Vornado Realty Trust | 350 Park Avenue (developing), 280 Park Avenue (JV) | large Midtown portfolio | Trophy / Class A, 10,000+ SF |

| BXP (Boston Properties) | The GM Building (767 Fifth), 399 Park Avenue, 601 Lexington | large national portfolio | Class A / Trophy, 10,000+ SF |

| Tishman Speyer | 300 Park Avenue; developed 270 Park Avenue | large Midtown portfolio | Class A, 10,000+ SF |

| RFR Realty | 375 Park Avenue (Seagram Building) | several M SF across Midtown | Class A / Trophy, 5,000+ SF |

| Rudin Management | 345 Park Avenue, 350 Park Avenue (partner) | ~10M+ SF | Class A, 5,000+ SF |

| L&L Holding | 425 Park Avenue | several M SF | Trophy, 10,000+ SF |

| The Soloviev Group | 9 West 57th Street (Solow Building) | ~1.5M SF here | Class A / Trophy, 10,000+ SF |

Portfolio figures are approximate. Several landlords listed (SL Green, Vornado, BXP, Tishman Speyer) hold much larger portfolios across Midtown, Midtown South, and Downtown. Metro Manhattan internal research (May 2026).

Transit here is strong on the subway side, and on the south end it adds commuter rail, which Columbus Circle does not have. The 4, 5, and 6 run along Lexington, the N, R, and W stop at Fifth and 59th, the E and M serve 53rd, and the F and Q reach 57th and 63rd. Near Park Avenue and the high 40s, Grand Central is a short walk away, which brings Metro-North and the LIRR’s Grand Central Madison within reach for suburban commuters. Our Commute Calculator and everyone’s home address will settle which areas work best.

| From | To the Plaza District | Mode |

|---|---|---|

| Upper East Side (72nd St) | 5 to 10 min | 4, 5, 6, or Q |

| Grand Central / Midtown core | 5 min | 4, 5, 6, or walk |

| Times Square | 8 to 12 min | N, Q, R, W, or shuttle + walk |

| Penn Station | 12 to 18 min | 1/2/3 to Times Sq + N/R/W, or bus |

| Downtown Brooklyn | 25 to 35 min | 4 or 5 |

| Long Island City, Queens | 15 to 25 min | E/M or N/W + transfer |

| Hoboken / Jersey City | 30 to 40 min | PATH to 33rd + subway |

| Newark, NJ | 35 to 45 min | NJ Transit to Penn + subway |

| Hicksville, NY (Long Island) | 50 to 60 min | LIRR to Grand Central + short walk |

| Stamford, CT | 60 to 70 min | Metro-North to Grand Central + short walk |

Plan on roughly $73.97/SF direct for standard Class A and about $103.14/SF once trophy buildings are in the mix (Metro Manhattan, August 2025). Transwestern put the submarket’s Class A average at $92.01/SF in Q4 2025, and at the end of March 2026 the Plaza District’s overall average reached $94.53/SF, the highest of any office submarket in the city (Yardi, Q1 2026). The very best Park and Fifth Avenue trophy floors ask from $150/SF into the $200s.

Standard Class A asked about $73.97/SF direct as of August 2025, with the Class A aggregate at $103.14/SF once trophy product is folded in (Metro Manhattan, August 2025); Transwestern’s Q4 2025 Class A average was $92.01/SF. Park Avenue and Fifth Avenue set the high end, while Madison and the Third/Lexington edge come in well below. For context, Midtown’s Class A average was $85.28/SF in Q1 2026 (Cushman & Wakefield, April 2026).

The Plaza District has the largest concentration of finance and law tenants in the city, the trophy buildings on Park and Fifth, and a Central Park frontage, while very little new space becomes available. Midtown’s prime vacancy fell to 2.9% in the first quarter of 2026 (CBRE, Q1 2026), and trophy availability has not risen in a quarter since early 2023 (Newmark, Q4 2025). Tight supply and steady demand keep its rents the highest in the city.

The Plaza District’s availability rate was about 10.4% in Q4 2025, among the tightest in Midtown alongside Penn Plaza at 9.9% (Transwestern, Q4 2025). The trophy tier is far tighter than that headline, effectively sold out, while the older Class B and value stock on the eastern edge carries the most space. For reference, Manhattan’s overall availability was 13.7% in Q1 2026 (Colliers, Q1 2026).

Finance and law both concentrate on Park Avenue and Fifth. On Park, 270 Park (JPMorgan), 345 Park (Blackstone), 425 Park (Citadel), and the Seagram Building anchor the corridor; on Fifth, the GM Building and 9 West 57th carry the marquee finance and law tenants (Metro Manhattan internal research, May 2026). Madison Avenue and the Third/Lexington edge handle the boutique and value-seeking firms in the same verticals.

Yes, by a wide margin on the trophy end. The Plaza District’s Class A aggregate is $103.14/SF, against $93.37/SF direct for Grand Central and $89.78/SF aggregate for Columbus Circle (Metro Manhattan, August 2025). If you want a Midtown address for less, Columbus Circle and Grand Central both come in cheaper, and Downtown Manhattan and the Financial District go far lower still.

Look at the eastern edge along Third Avenue and Lexington and a few boutique Madison Avenue towers, where older Class A and renovated Class B floors price below the trophy line (Metro Manhattan internal research, May 2026). Flex and coworking operators run space across the submarket, and a thin pool of sublets occasionally opens up. Most small tenants will still pay more here than in almost any other Midtown submarket, so weigh the prestige against the rent.

Class mostly tracks a building’s age, systems, and prestige. Here, trophy and Class A means the Park and Fifth Avenue towers and the renovated stock around them, while Class B and the little Class C there is means the older prewar and postwar buildings on Madison, the side streets, and the Third/Lexington edge. A well-renovated Class B floor in the Plaza District can hold its own against Class A in most other neighborhoods, for less.

Two Foster + Partners towers are in the pipeline. JPMorgan opened its 2.5-million-SF global headquarters at 270 Park Avenue in October 2025 (JPMorganChase, October 2025), and Vornado, Rudin, and Citadel plan to break ground on 350 Park Avenue, a roughly 1.85-million-SF, 1,600-foot tower anchored by Citadel, with demolition scheduled for spring 2026 and delivery around 2032 (The Real Deal, February 2026). Both are largely committed, so neither adds available space for tenants searching now.

The big names are SL Green and Vornado (the two largest office owners in the city, jointly holding 280 Park), BXP (the GM Building and 399 Park), RFR (the Seagram Building), Rudin (345 Park and a partner on 350 Park), L&L Holding (425 Park), Tishman Speyer (300 Park, and the developer of 270 Park), and the Soloviev Group (9 West 57th) (Metro Manhattan internal research, May 2026).

The submarket has extensive subway service: the 4, 5, and 6 on Lexington, the N, R, and W at Fifth and 59th, the E and M at 53rd, and the F and Q at 57th and 63rd. Its southern end near Park Avenue is a short walk from Grand Central, so Metro-North and the LIRR’s Grand Central Madison serve suburban commuters as well. That combination of subway and commuter rail is an advantage over subway-only submarkets like Columbus Circle.

Much of the best Plaza District space, especially the rare trophy blocks and the quiet subleases, never hits the public listing sites, and a tenant broker gets you to it (and to who is actually dealing). The landlord pays the commission, so it costs a tenant effectively nothing. Before you tour, skim the essentials to ask before leasing NYC office space and get familiar with the Good Guy Guarantee most NYC landlords want smaller tenants to sign.

Accessibility Tools